The Fuse

Equity futures are a bit soft this morning after a hangover of earnings last night. Tesla and Netflix along with Taiwan Semi reported good numbers but not enough to push their stocks higher. As a result, technology is selling off this am, nearly 1%. After the huge run these stocks have had maybe a bit of a breather is in order. We are in a seasonally weak period for stocks with a big expiration day tomorrow.

Interest Rates are up modestly this morning as investors are shunning bonds a bit. Next week’s Fed meeting is going to tell us plenty about the outlook for fixed income.

Not much news overnight but inflation in Hong Kong slid a bit. Earnings from JNJ this morning topped estimates, yesterday several strategists lowered their forecast for a recession and increased the US economy’s chances for a soft landing. Though the Fed continues to raise rates which could tip the economy into recession, so far GDP estimates for Q2 remain well above 2%, the first half of the year above 2% annualized. The economy would have to fall off a cliff in the second half, and with the stock market already strong, this leading indicator does not see it happening.

Strong earnings as you might have expected from Tesla, Netflix and IBM but these stocks may have seen their best days already. Let’s see how the market interprets earnings and guidance over the coming days, but no doubt Tesla and Netflix have been distributing gifts this year.

A continuation of the recent rally with very good internals and statistics. Another close above some significant resistance (4,550) was passed today, and with only about 5% left to get the SPX 500 to an all time high, we look for clues that might get us there. One of them is cumulative breadth.

Breadth was positive today but fell short of yesterday’s terrific run. The oscillators are now back to overbought and may move a touch higher before a bigger selloff ensues – just in time for the next Fed meeting?

Volume trends were moderate as market players digested the prior day’s strong gains. We could see a resurgence in turnover as bigger news items break this week (earnings, economic data).

A fairly strong effort to push the SPX above 4,600 failed to happen Wednesday, but that objective is certainly in sight. Support remains strong at 4,500, the Dow Industrials now see good support at 35K.

The Internals

What’s it mean?

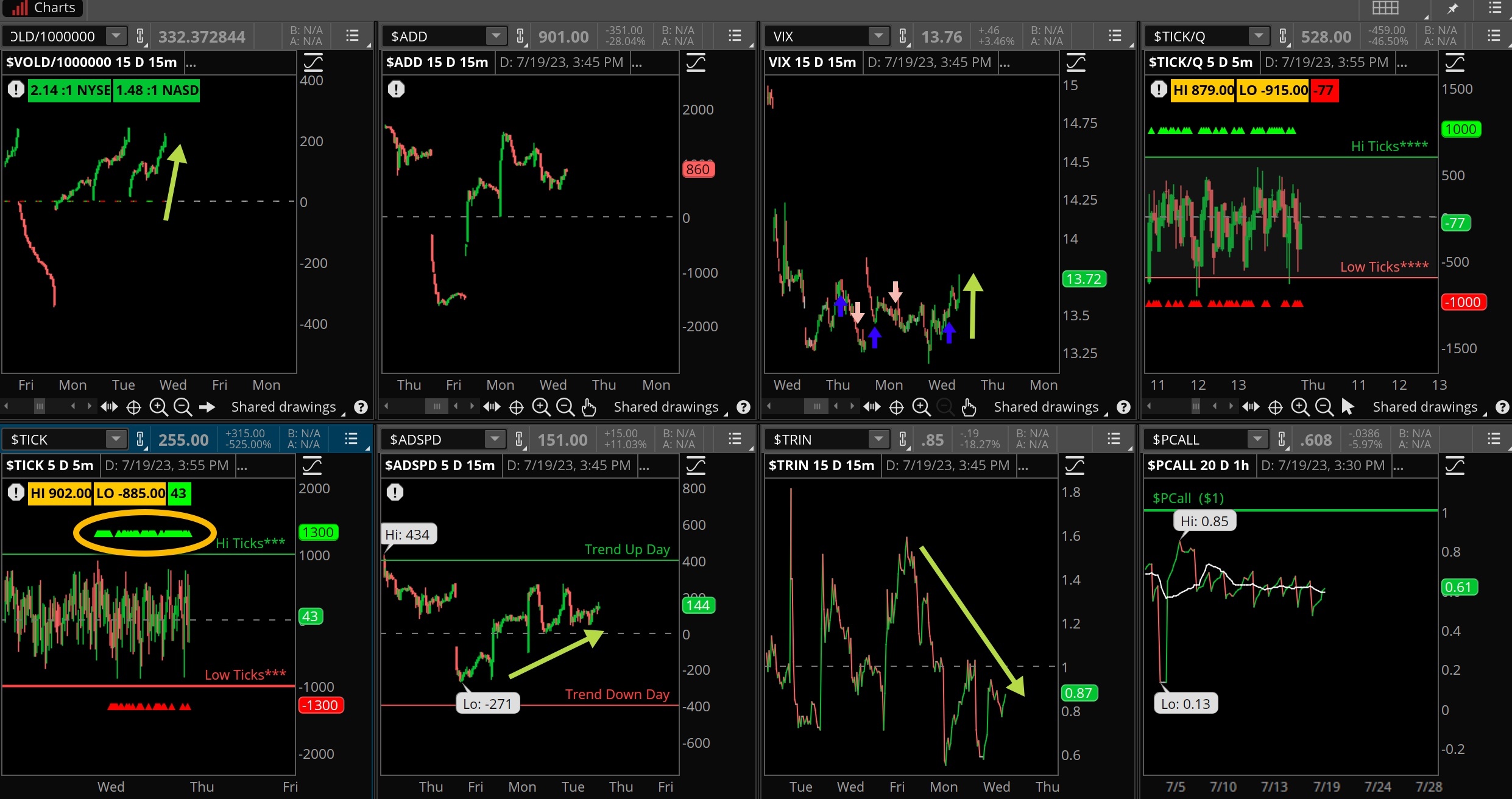

Following yesterday’s sharp move higher we were looking for some softness, yet the buyers were still engaged early on. Notice the strong VOLD all day long and finished at the highs of the session. VIX was higher though, reflecting some worry about a complacent market. Ticks were strong most of the session while the ADSPD is showing a nice trend. We want to watch how the market finishes on Friday to determine what might come in the last week of July trading.

The Dynamite

Economic Data:

- Thursday: Jobless claims, philly fed index, leading indicators, home sales

- Friday:

Earnings this week:

- Thursday: AAL, DHI, JNJ, NOK, TSM, CSX, PPG, VMI

- Friday: AXP, AN

Fed Watch:

Fed funds futures at 99.8% probability of a hike next week as of today. Fed speakers will be quiet this week in front of the next FOMC meeting. Current odds favor a rate hike at the next meeting but certainly the cooler inflation may offer the committee yet another opportunity to pause. So many hikes in the system seem to be working their magic, and if the economy holds up strong we’ll see rate cuts coming in 2024.

Issues/Stocks to Watch this Week

Earnings – Companies will start reporting their quarter this week, a bigger list of names henceforth. We are getting a sampling of tech earnings and other groups this coming week.

Volatility – VIX remains very low and as we have preached in prior weeks, it is dangerously low. That said, until a change in character is seen there is no reason to fight the trend.

Tesla – the big EV car company reports on Wednesday evening, it is always entertaining to hear Elon Musk on the call and how well the company is doing.