The Fuse

Futures are rebounding Friday morning after getting pounded yesterday. The result with the Nasdaq down over 2% but the Industrials higher by .5%, thanks to gains in JNJ and GS. With a pending rebalance in the Nasdaq Monday and a fed meeting upcoming we are seeing some repositioning.

Interest Rates are modestly lower today as bonds are looking a bit more appealing.

Overnight the UK brought in better than expected retail sales. Transportation stocks hit a 52 week high yesterday as this group remains quite strong. Today is a huge July options expiration day.

American Express and Schlumberger reported strong earnings but missed on the revenue, but did either guide in line or slightly higher for 2023.

Roper also reported strong earnings/revenue and raised guidance.

Not too many events but a rebalancing of the Nasdaq will weigh on peoples’ minds over the weekend. What’s it mean? Basically the bigger names in the Nasdaq (Apple, Microsoft, NVIDIA, etc) will have a smaller weighting as to have lesser influence in the movement of the index. In the end, after the rebalance it won’t much matter.

Modestly negative breadth yesterday but a respite was deserved. We have seen some pretty strong breadth days over the last couple of weeks, cumulative breadth is not far from an all time high.

Volume was elevated in anticipation of the July options expiration today. We’ll see more volume come in by the end of the day. Next week should also bring us more turnover with a big earnings week and Fed decision.

Are we seeing a stall out here? Perhaps for a short while the indices need to digest recent gains. If you’re bullish, that’s a positive situation. With about 7 trading days left in July the SPX 500 is up nicely for the month, and if it can stick positively it would be five straight up months and a potentially important turn towards a bull market (end of August).

The Internals

What’s it mean?

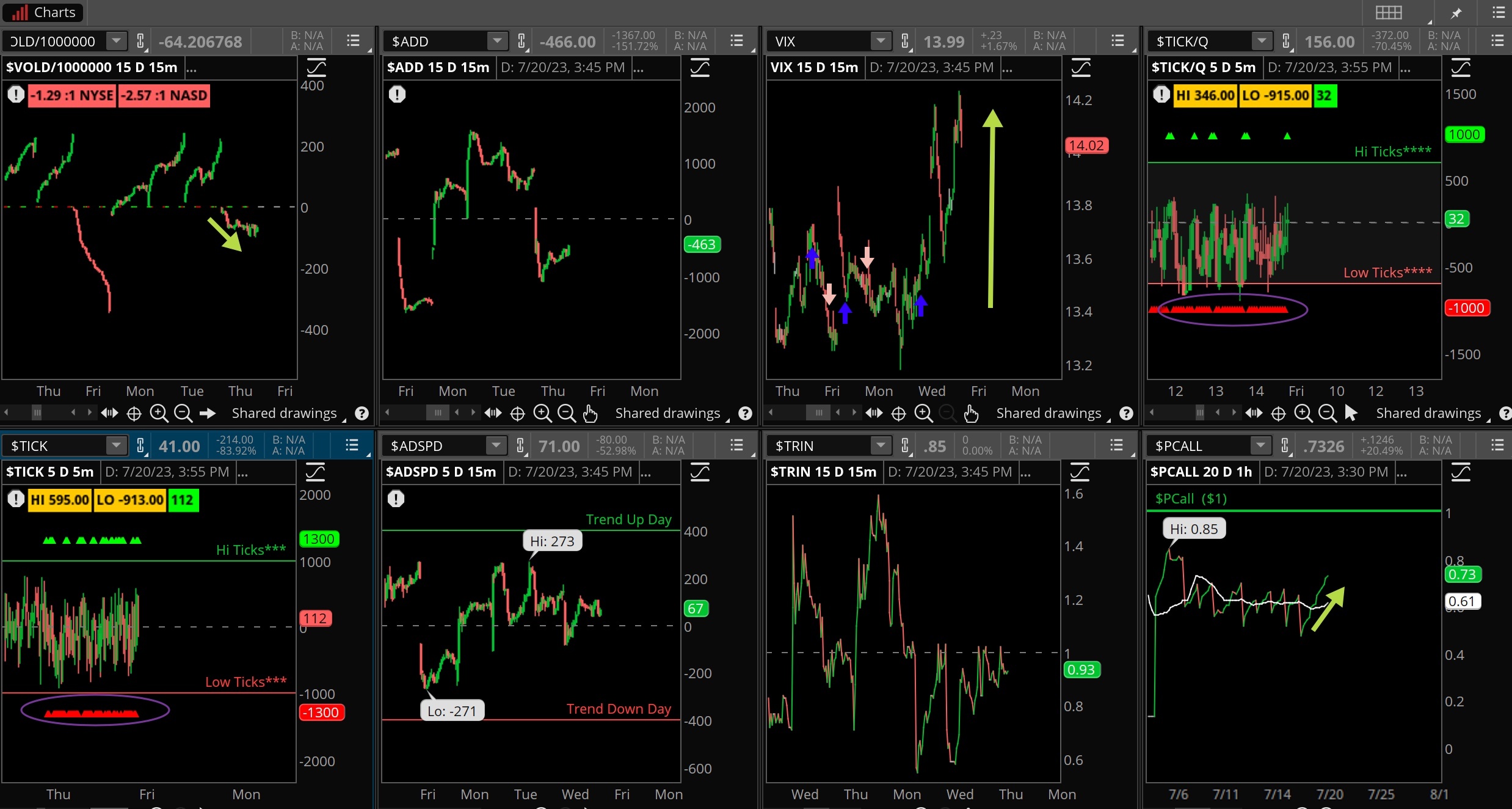

Breadth took a breather on Thursday, notice how the VOLD was down but did not accelerate into the close as it did last Friday. So, it could indicate just a one day selling event and that’s it. Volatility rose up sharply, if you want to call it that to 14% and is trying to establish a bottom. We are in a seasonally weak period for stocks and with a converging situation (Fed, earnings) it means stocks can/will be sold. Ticks were pretty concentrated in red yesterday, something to watch for.

The Dynamite

Economic Data:

- Friday: n/a

Earnings this week:

- Friday: AXP, AN

Fed Watch:

The Fed balance sheet continues to shrink, down another 22 billion this week. Fed funds futures at 99.8% probability of a hike next week as of today. Fed speakers will be quiet this week in front of the next FOMC meeting. Current odds favor a rate hike at the next meeting but certainly the cooler inflation may offer the committee yet another opportunity to pause. So many hikes in the system seem to be working their magic, and if the economy holds up strong we’ll see rate cuts coming in 2024.

Issues/Stocks to Watch this Week

Earnings – Companies will start reporting their quarter this week, a bigger list of names henceforth. We are getting a sampling of tech earnings and other groups this coming week.

Volatility – VIX remains very low and as we have preached in prior weeks, it is dangerously low. That said, until a change in character is seen there is no reason to fight the trend.

Tesla – the big EV car company reports on Wednesday evening, it is always entertaining to hear Elon Musk on the call and how well the company is doing.