The Fuse

Equity futures are rising modestly this mornings as the market works off a hangover from last Friday’s heavy options expiration day.

Rates are moving lower as interest in bonds perks up. We’ll see bond prices moving around quite a bit this week before/after the Fed decision.

Stocks were only slightly changed Friday but the Industrials did manage to score 10 straight winning sessions. Overnight, many European global PMI data were lower than expected, which continues a trend of weaker data in that region.

Decent earnings from Domino’s (DPZ) this morning while Chevron (CVX) pre-announced upside guidance. We’ll hear from NXPI, CLF, LOGI, WHR later this afternoon and VZ, GM, MMM, GE, SPOT and nUE among others in the am.

Plenty of stuff happening this week including earnings news, Fed moves, and economic data.

Breadth had been pretty strong leading up to Friday but backed off significantly. That’s not a horrible situation, even the buyers run out of fuel at times and need to reset.

Volume levels were elevated as option expiration exaggerated the ending moves. We may see a big more flowing turnover today and into midweek, but for now the markets are fairly balanced between buyers/sellers (not much advantage to either side currently).

We remain steadfast that 4,500 is good support on the SPX 500 and below there all the way down to 4,350 should a break occur. For the Nasdaq, 15K is solid support (3% lower).

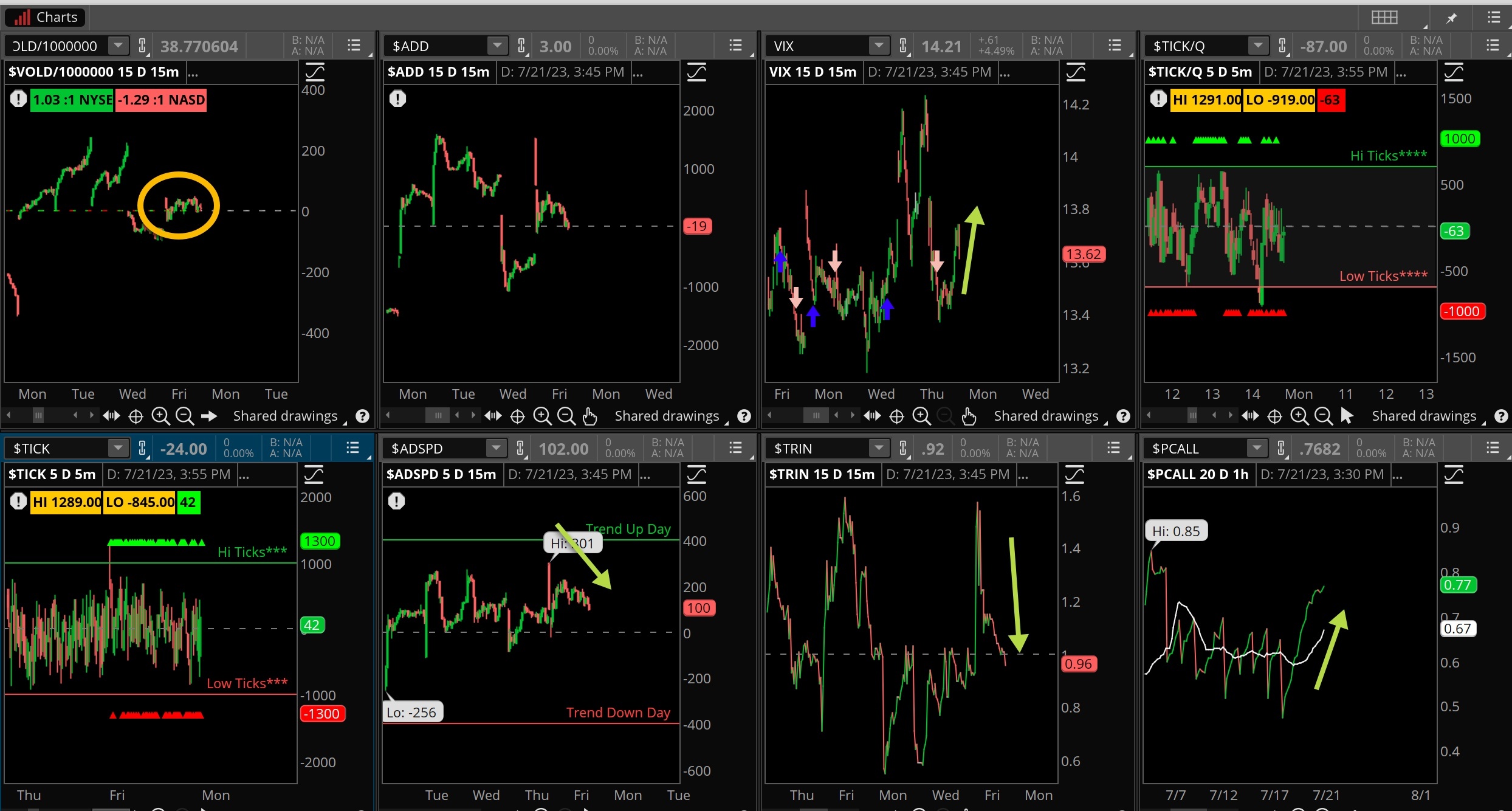

The Internals

What’s it mean?

We could call Friday’s action ‘blah’. Really not much to consider as options expiration took center-stage. What that means is buyers and sellers had a stalemate working, and we can see it reflected in the octagon. VOLD had a negligible move, VIX up a bit as were put/calls but other trend indicators were mostly on the flat line. A solid mix of ticks as well, call it a ‘rest day’ for traders.

The Dynamite

Economic Data:

- Monday: PMI Flash

- Tuesday: home price index, case/shiller, richmond fed manufacturing

- Wednesday: New home sales, FOMC announcement, investor confidence index

- Thursday: GDP Q2 first look, jobless claims, inventories, KC Fed

- Friday: Consumer sentiment, employment cost index, income/outlays

Earnings this week:

- Monday: NXPI, WHR, LOGI, FFIV

- Tuesday: VZ, MMM, GM, SPOT, NUE, RTX, MSFT, GOOGL, SNAP, V, TDOC, TXN

- Wednesday: T, BA, KO, TMO, HLT, ADP, UNP, META, CMG, NOW, LRCX, EBAY MAT

- Thursday: MCD, RCL, LUV, MA CROX, F, INTC, ROKU, FSLR, BMY, HON, VLO, TMUS, ENPH

- Friday: CVX, XOM, CEN, AZN, PG, CHTR

Fed Watch:

A big Fed meeting later this week as the committee is expected to resume rate hikes. Rather than taking another pause, market players are predicting with certainty the Fed will raise the funds rate to 5.25%, a 1/4 point move higher. The FOMC is not likely to disappoint and deliver higher rates and perhaps point to another hike later in the year.

Stocks to Watch

Big tech – HUGE week of earnings for big tech names, we’ll see how they fare and if prices are already baked into good news.

VIX — The fear index remains muted but is likely to rise in front of the Fed decision. If so, we’ll see if volatility sellers come out and smash the VIX lower.

Sentiment — Extreme sentiment now with many of the surveys/polls telling us investors/traders have become very bullish. That’s not a tragedy for the trend, but when it shifts there is likely going to be some pain and frustration.