The Fuse

Futures are rising a bit this morning as traders/investors prepare for some big earnings after the close from Microsoft, Alphabet and Visa.

Also, the Fed’s next meeting starts later today, concluding tomorrow with a policy decision.

Interest Rates are higher slightly today as bond traders position themselves for some volatility. We are seeing a narrowing of the yield curve once again but the inversion is still looking ominous, with a potential recession on the way.

The Fed meeting starts today and will conclude tomorrow. A 25bp hike is expected but it’s the wording/language and press conference that will be on everyone’s mind. Oil surged yesterday on strong demand from China. The Dow Industrials have now risen 11 straight sessions.

Strong earnings this morning from GE, MMM and GM are buoying the markets so far. Bigger tech names a bit later on today. Raytheon and Nucor are a bit of a drag.

Plenty of stuff happening this week including earnings news, Fed moves, and economic data.

Better breadth yesterday but clearly the buyers are not stepping up with vigor. Banks and energy led the parade higher Monday but it was not all that convincing. We did see new highs expand which is a bullish development.

Volume receded on Monday after a big July expiration finished up. It was somewhat expected and we’ll see some big volume prints later in the week after the Fed announcement and big tech earnings.

The drive towards 4,600 on the SPX 500 continues, and that may be target before the end of the month.

What’s it mean?

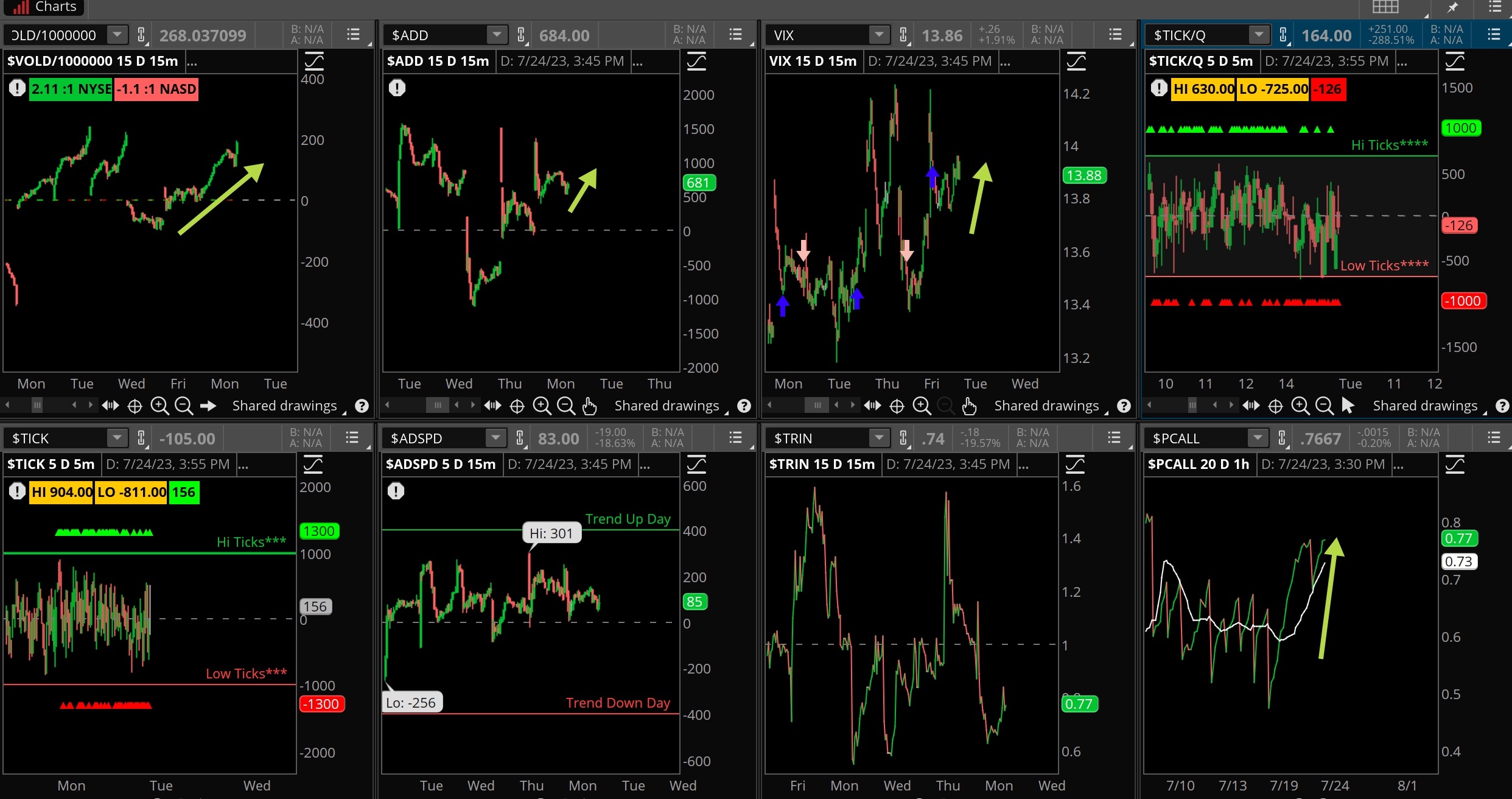

It was a grind and tough for the bulls to manage but they pulled it off. Another strong performance from the broader market and the Dow Industrials, notice the stronger VOLD but not as convincing as prior weeks. ADD was strong and the VIX actually climbed a bit, reflecting some worry before some earnings hit the tape later today. Put/call is rising again, something that we’ll have to pay close attention to, it can be a leader to the downside if more put volume is seen.

The Dynamite

Economic Data:

- Tuesday: home price index, case/shiller, richmond fed manufacturing

- Wednesday: New home sales, FOMC announcement, investor confidence index

- Thursday: GDP Q2 first look, jobless claims, inventories, KC Fed

- Friday: Consumer sentiment, employment cost index, income/outlays

Earnings this week:

- Tuesday: VZ, MMM, GM, SPOT, NUE, RTX, MSFT, GOOGL, SNAP, V, TDOC, TXN

- Wednesday: T, BA, KO, TMO, HLT, ADP, UNP, META, CMG, NOW, LRCX, EBAY MAT

- Thursday: MCD, RCL, LUV, MA CROX, F, INTC, ROKU, FSLR, BMY, HON, VLO, TMUS, ENPH

- Friday: CVX, XOM, CEN, AZN, PG, CHTR

Fed Watch:

A big Fed meeting later this week as the committee is expected to resume rate hikes. Rather than taking another pause, market players are predicting with certainty the Fed will raise the funds rate to 5.25%, a 1/4 point move higher. The FOMC is not likely to disappoint and deliver higher rates and perhaps point to another hike later in the year. More importantly is the statement and the follow-on press conference by Chair Powell.

Stocks to Watch

Big tech – HUGE week of earnings for big tech names, we’ll see how they fare and if prices are already baked into good news.

VIX — The fear index remains muted but is likely to rise in front of the Fed decision. If so, we’ll see if volatility sellers come out and smash the VIX lower.

Sentiment — Extreme sentiment now with many of the surveys/polls telling us investors/traders have become very bullish. That’s not a tragedy for the trend, but when it shifts there is likely going to be some pain and frustration.