The Fuse

Equity futures are down modestly as investors show less of a risk appetite on Fed day. It makes sense after the markets have been on such an upward trajectory this month. The Industrials are now at a twelve session winning streak, but that may end this week.

Interest Rates are tight this morning as the investing world awaits word on fed monetary policy. The statement will be important but also the Chair’s comments following, too. Markets are expecting a rate hike today of 25bps and perhaps a pause thereafter. Regardless, we are coming to the end of a rate hiking cycle.

It’s Fed day of course, we’ll be listening carefully to the Chair’s comments. The economy has been resilient this year, reflected in a strong stock market where three of four indices are up double digits for 2023. Yet, policymakers have a history of overshooting just to be sure inflation is falling, and that could be the policy error many are worried about.

Solid earnings this morning from Industrial names Boeing and Coke have those names pushing higher, but volatility is up a bit in front of an important Fed decision. Last evening had solid earnings reports from Google and Microsoft, but the latter showed some weaker guidance going forward and is down sharply. Meta will report earnings tonight along with Chipotle, Lam Research and eBay.

The day of reckoning has arrived: New Fed Policy will be announced, and likely higher interest rates.

Breadth was even on the day as sellers continue to find an excuse to dump stocks. There are a million reasons to sell of course, only one reason to buy.

Volume trends are starting to improve as we suspected they would as we approach the end of the month. Certainly with a Fed decision coming up later today re-positioning in stocks and fixed income will be a top priority.

The 4600 level was breached by the futures market and closed above there but remains elusive to the SPX cash. However, it seems a pretty small move from here, and with some positive sentiment to end the month on a high note that 4,600 level will be broken soon enough.

What’s it mean?

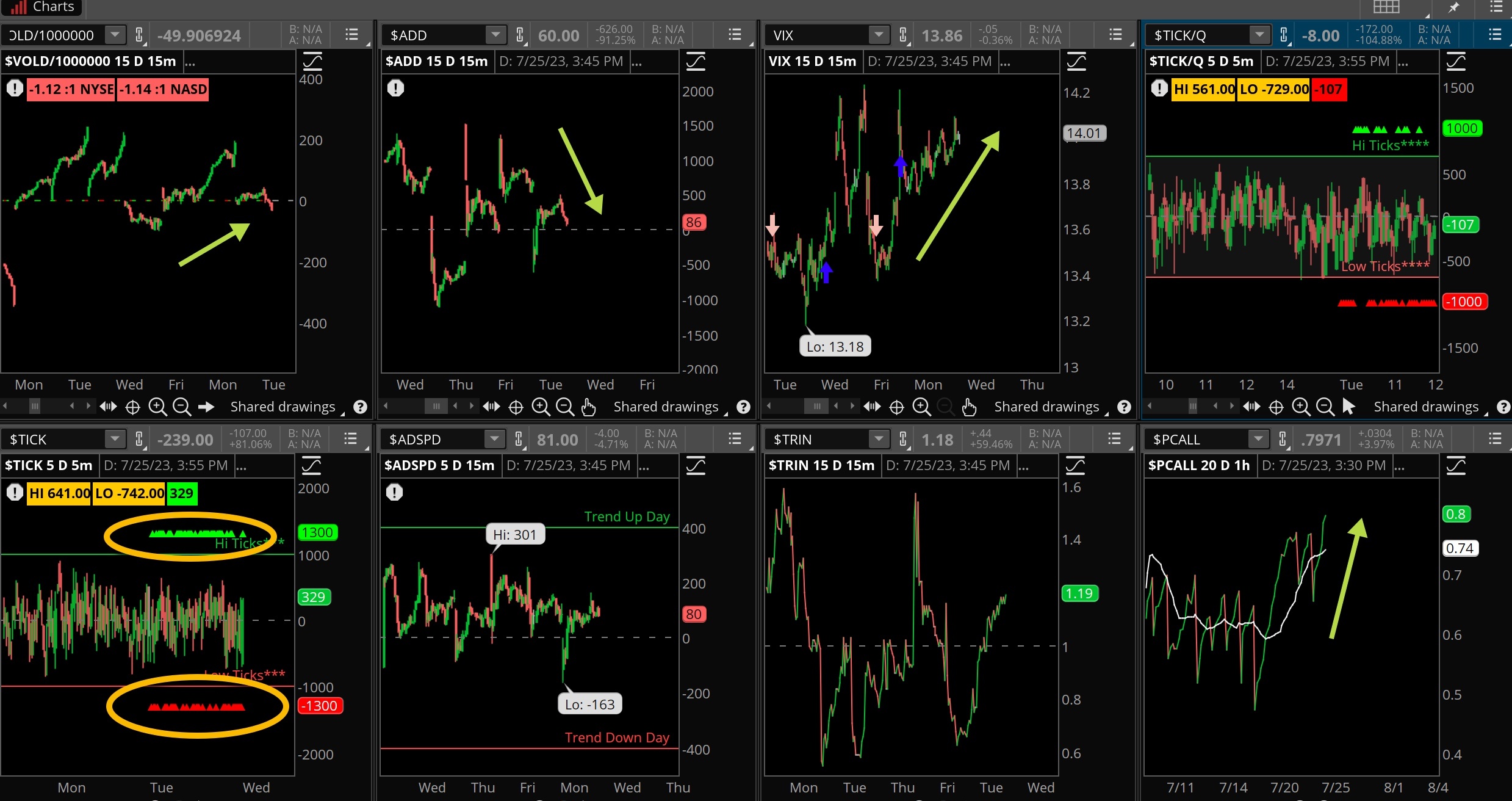

A slow session but quite a few positives to extract. The indicators on the octagon really do not tell how price action developed, and that is not uncommon. In fact, we saw the VOLD barely down along with the ADD, a virtual stalemate between buyers/sellers. The ticks show the story too, pretty much even across the board.

VIX is climbing though as are put/calls, so clearly some market players are looking to buy some protection. It makes sense.

The Dynamite

Economic Data:

- Wednesday: New home sales, FOMC announcement, investor confidence index

- Thursday: GDP Q2 first look, jobless claims, inventories, KC Fed

- Friday: Consumer sentiment, employment cost index, income/outlays

Earnings this week:

- Wednesday: T, BA, KO, TMO, HLT, ADP, UNP, META, CMG, NOW, LRCX, EBAY MAT

- Thursday: MCD, RCL, LUV, MA CROX, F, INTC, ROKU, FSLR, BMY, HON, VLO, TMUS, ENPH

- Friday: CVX, XOM, CEN, AZN, PG, CHTR

Fed Watch:

A big Fed meeting later this week as the committee is expected to resume rate hikes. Rather than taking another pause, market players are predicting with certainty the Fed will raise the funds rate to 5.25%, a 1/4 point move higher. The FOMC is not likely to disappoint and deliver higher rates and perhaps point to another hike later in the year. More importantly is the statement and the follow-on press conference by Chair Powell.

Stocks to Watch

Big tech – HUGE week of earnings for big tech names, we’ll see how they fare and if prices are already baked into good news.

VIX — The fear index remains muted but is likely to rise in front of the Fed decision. If so, we’ll see if volatility sellers come out and smash the VIX lower.

Sentiment — Extreme sentiment now with many of the surveys/polls telling us investors/traders have become very bullish. That’s not a tragedy for the trend, but when it shifts there is likely going to be some pain and frustration.