The Fuse

Equity futures are rising sharply this morning following the Fed’s latest move. The rate hike that came yesterday was the 14th straight hike since March 2022, the highest fed funds rate since 2002. Even with the high cost of funds, equity players still believe stocks are the only game in town.

Interest Rates are slightly higher today after only a moderate move following the new Fed policy change. We may see rates remain steady as bond volatility has been weaker than normal.

GDP for Q2 will be out later this morning and the ECB will make a decision on monetary policy as well. Stocks are poised to make a run toward all time highs very soon, yet once August gets started next week it could be a tough summer of weaker trade following a positive month.

Another solid earnings beat for Meta has this stock rallying sharply, near 9% early morning. We also saw good earnings from ALGN and LRCX last night, this morning brings MCD, MA, HON and LUV as well as VLO and ABBV. Tomorrow am is PG, XOM, CVX. A very busy schedule.

The Fed raised rates yesterday as expected but left the door open to be flexible with policy. Chair Powell reiterated his stance to pay attention to the data and respond accordingly. Later today we’ll have a decision from the ECB where they are also expected to raise interest rates. The dollar is rallying on both pieces of news, gold is above 2,000 per ounce and firming up while crude is also higher.

Better breadth again Wednesday but mostly driven by the small caps again. We don’t quibble on how it’s done, just that it is done. Breadth indicators are on a buy signal.

Volume continues to improve as buyers are still flocking towards stocks. Yesterday had plenty of volatility before and after the Fed decision, with sharp moves up and down but within a 1% range. Nasdaq remains very strong as earnings are supporting that index. We continue to see good money flows into small caps as well, the volume indicator for the Russell 2K is bullish.

It’s mission impossible for the SPX 500 as the index tries once again to close above 4,600. If today’s opening rally holds firm this could be the day, but we would like to see good statistics to support the move and of course, followthrough. It seems the calendar is helping out too, with Monday being the last day of the month and money flows piling in day after day.

What’s it mean?

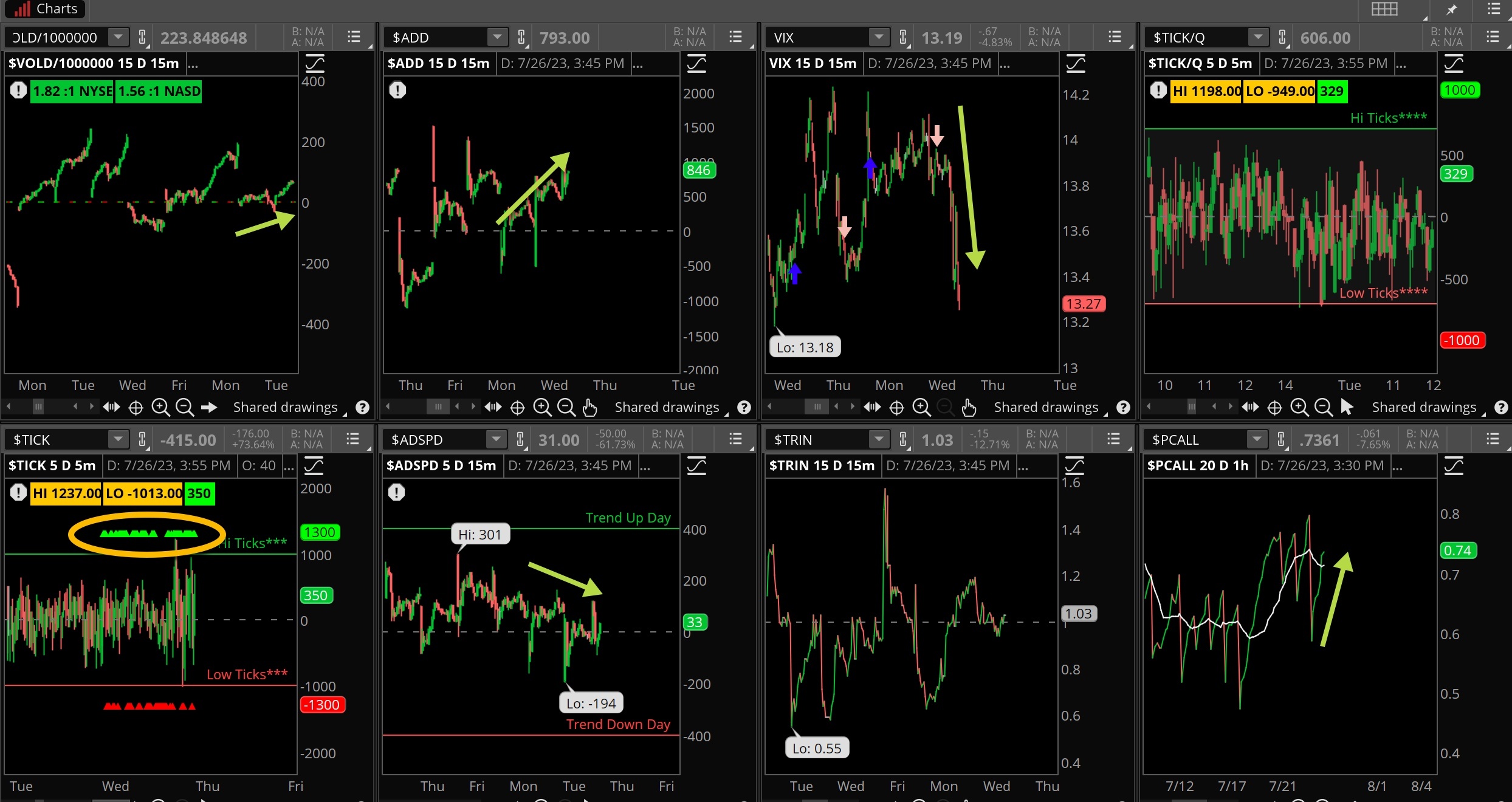

The octagon is not showing too much here from yesterday’s action. One would think volatility would rise up but remember, when news is released as it was yesterday there is a big drop in VIX, as we see above. VOLD also ticked in for a positive while ADD finished much higher, too. TICKS were moderate too, while put/call is also higher but not screaming sell.

The Dynamite

Economic Data:

- Thursday: GDP Q2 first look, jobless claims, inventories, KC Fed

- Friday: Consumer sentiment, employment cost index, income/outlays

Earnings this week:

- Thursday: MCD, RCL, LUV, MA CROX, F, INTC, ROKU, FSLR, BMY, HON, VLO, TMUS, ENPH

- Friday: CVX, XOM, CEN, AZN, PG, CHTR

Fed Watch:

The committee met Wednesday to discuss a new policy move and raised rates as expected by 25bps. The also left the door open for another rate hike or a pause, and that means the Fed is trying pivot away from a bold hawkish view. Rate cuts? Not for quite a long time and until the committee sees inflation falling further towards their 2% objective. Chair Powell said he did not see that happening until at least 2025, so it could be higher for much much longer.

Stocks to Watch

Big tech – HUGE week of earnings for big tech names, we’ll see how they fare and if prices are already baked into good news.

VIX — The fear index remains muted but is likely to rise in front of the Fed decision. If so, we’ll see if volatility sellers come out and smash the VIX lower.

Sentiment — Extreme sentiment now with many of the surveys/polls telling us investors/traders have become very bullish. That’s not a tragedy for the trend, but when it shifts there is likely going to be some pain and frustration.