The Fuse

Futures are falling this morning after some weakness overnight in Asian markets. This follows the read from the FOMC minutes (June 13/14 meeting) that said the committee was likely raise rates further, and there was a consensus view of that hawkishness.

Interest Rates continue to creep higher and towards 4% on the ten year. Either the bond market sees strong growth or inflation is going to run even higher.

Big news from Meta as they released their twitter competitor ‘Threads’ last night. It was a huge opening, the stock is higher this morning after rising sharply (more than 3%) yesterday.

Not much on the earnings front this week other than LEVI.

Short trading week but we’ll be paying attention to market volatility

Working off that overbought condition, breadth was pretty weak all session long, another day or two to burn off the overbought reading is likely.

Volume trends remain mediocre as the indices continue to digest a recent run higher.

We still see 4400 as good support to the downside on the SPX 500 with a new target of 4500-4535. Nasdaq performed well today, if there is some followthrough we’ll have more upside to go.

The Internals

What’s it mean?

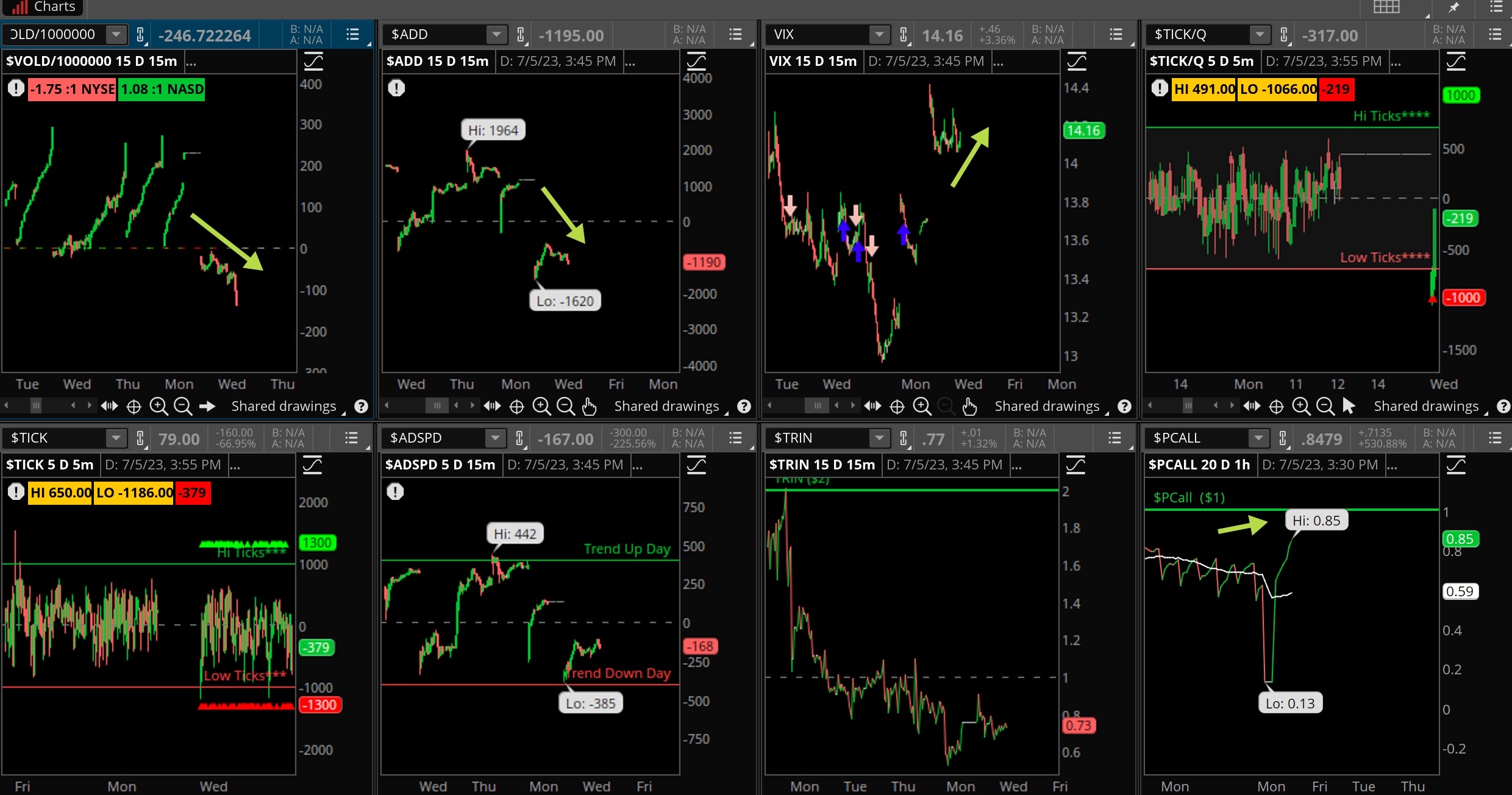

Volatility rose up some yesterday in a ‘payback’ fashion for the drop in vol in Monday’s half session. Notice the bounce back in the put/call ratio yesterday, but VOLD and ADD were not inspired at all by Monday’s rally. However, we did finish off the lows of the session, ticks were moderate and the VIX did finish off its highs. We are in summer trading mode now.

The Dynamite

Earnings This Week:

- Thursday: LEVI

- Friday: AZZ

Economic Data this week:

- Thursday: Jobless claims, JOLTS report, ISM non-manufacturing, service PMI

- Friday: Non-farm payroll report

Fed Watch:

The Fed’s John Williams spoke yesterday and stated price pressures are still too high, but there are some positives. This week’s job report will go a long way in determining how many more hikes are needed.

Stocks to Watch

Tesla – strong numbers out over the weekend might stoke a big rally for the EV car maker.

Semiconductor Stocks – As we heard last week, the Biden Administration is going to make it difficult for US companies to sell AI chips into China.

We’ll see if there is any followthrough.

Volatility – Again watching the VIX here as the holiday shortened week may carry some surprises, especially with an important jobs number coming up Friday.