The Fuse

Equity futures are sliding a bit this morning as the fallout from yesterday’s harsh statement from the Fed is digested. The committee passed on hiking rates yesterday for the first time in this hiking series but warned there could be more out there by the end of the year.

Rates are modestly higher this am after taking a dive following the new fed policy statement. The term structure of rates is still quite inverted and even expanded more on Wednesday. Eventually that will matter but for now equity investors are trusting the bond market./span>

Some estimates on rate hikes out today, some analysts are not believing the new Fed forecast calling for 2 more hikes this year. That’s quite the dare! China economic growth was downgraded. Overnight, China cut their depository rate in order to stimulate some demand. This morning the ECB will have a rate policy decision, they are expected to raise their funds rate by 25bps.

Earnings are out this morning on Kroger and Jabil, while after the close we’ll hear from mega cap tech name Adobe Systems, which has been on a roll of late. Lennar reported strong earnings last evening and raised guidance.

The Fed sided with the markets this week and left rates unchanged. The funds rate remains at 5%, but in the projections the committee members see more rate hikes ahead. Markets were volatile on that revelation.

Breadth was following through most of the day but sellers came out and took positions off the table after the fed decision. Following PPI this morning, buyers were in a mood to add but that soured later in the day.

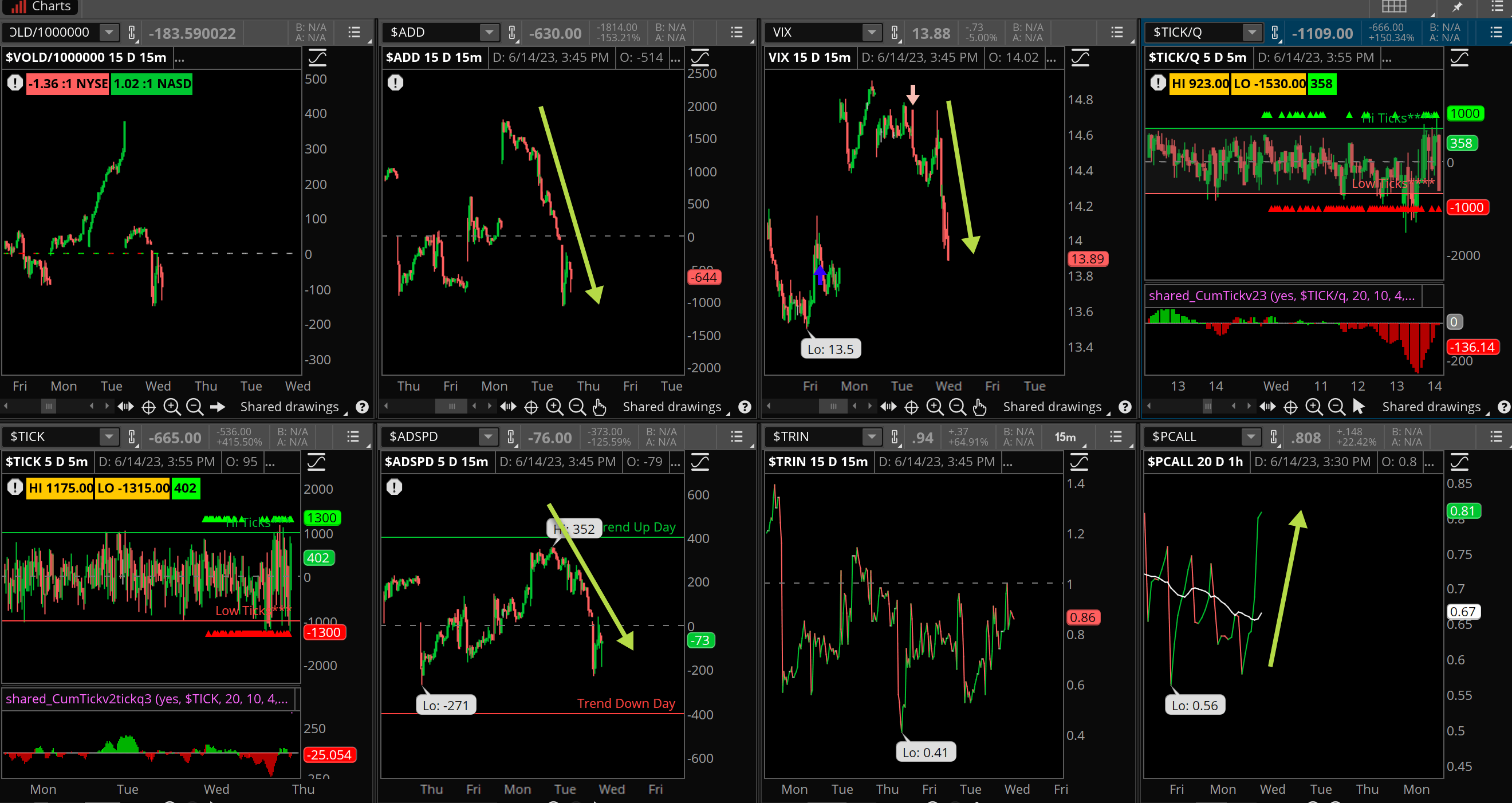

Volume was elevated once again today, we’ll notch this as barely an accumulation day, the Dow Industrials however was all about distribution, thanks to a big slide in UNH.

More gains for the indices as the road to 4400 is still on for the SPX 500. Lower rates on Wednesday after the Fed pause will stoke even more rallying in the Nasdaq names.

What’s it mean?

Check out the VIX here, falling sharply and nearly filling the gap from Monday. Three straight up sessions for the indices but only two good breadth days. VOLD and ADD were weak all day and closed near the lows, despite a big rally end of day. Put/calls raced higher too, protection was being bought and held.

The Dynamite

Economic Data:

- Thursday: Jobless claims, Retail Sales, Empire State manufacturing, Business Inventories

- Friday: Consumer Sentiment

Earnings this week:

- Thursday: JBO, KR, COGT, ADBE

- Friday: BHAT, BUFF, NATH, ONVO

Fed Watch:

It’s the most important Fed meeting this week since….the last one? Of course that is hyperbolic, but we should note as we move forward in time the discussion around the table during the Fed meetings will become more divided. Recent comments from Fed speakers tell us some are talking pause, while others see the need for more aggressive rate hike moves. We’ll learn more Wednesday and in the press conference with Chair Powell. In addition, the ECB will have a rate decision later in the week.

Stocks to Watch

VIX – Volatility has reached levels not seen since before the pandemic. Some say it is ‘too low’. However, it is simply an indicator that is reflecting the mood or temperature of the room.

Federal Reserve – A big meeting as mentioned above, with the strength recently in the stock market could a ‘sell the news’ follow the latest policy decision?

Inflation – Two reads on inflation this week and Retail sales. We’ll get a good view on how inflation is being worked through the system and if the Fed’s efforts of higher rates is actually paying off.

[thrive_leads id=’60674′]