The Fuse

Futures are soft today as the markets continue to tail from last Friday’s poor showing. On a big expiration day we tend to see a hangover effec, in addition volatility was smashed Friday and that ends up be ‘paid for’ the following few days after a holiday.

Interest Rates are slightly lower as we start the new week but the 10 yr remains stubbornly above 3.7%. Fed futures are

China cut interest rates last night in an effort to stimulate a weak economy, but inflation continues to rage hot in that region.

We’ll hear from FDX this week and ACN, DRI and KMX along with KBH. Not many but some important names as we head into the end of the quarter.

Not much on the event front this week as stocks look to take a breather. Several conferences are scheduled for the next couple weeks into the next holiday, July 4th. More news over cyber attacks on the rise, AI continues to be a driver of growth.

Breadth was poor all session long as the buyers simply did not step up. We had an overbought reading on breadth so a pullback here is not damaging. A few days in a row of bad breadth would set up a bearish scenario.

Volume levels were elevated on Friday due to the expiration of options Friday, a triple witching variety. We should see volumes remain higher for a few more days then settle down by the end of this week.

With an extended market it is hard to pinpoint just where the market is going to fall to. The Nasdaq has been riding high all year long with very few pullbacks, those with FOMO seem to be coming into the market on every dip. Still, we have discipline here, so the 20 moving average, rising everyday is where we should find good support (currently 4260 on the SPX 500).

The Internals

What’s it mean?

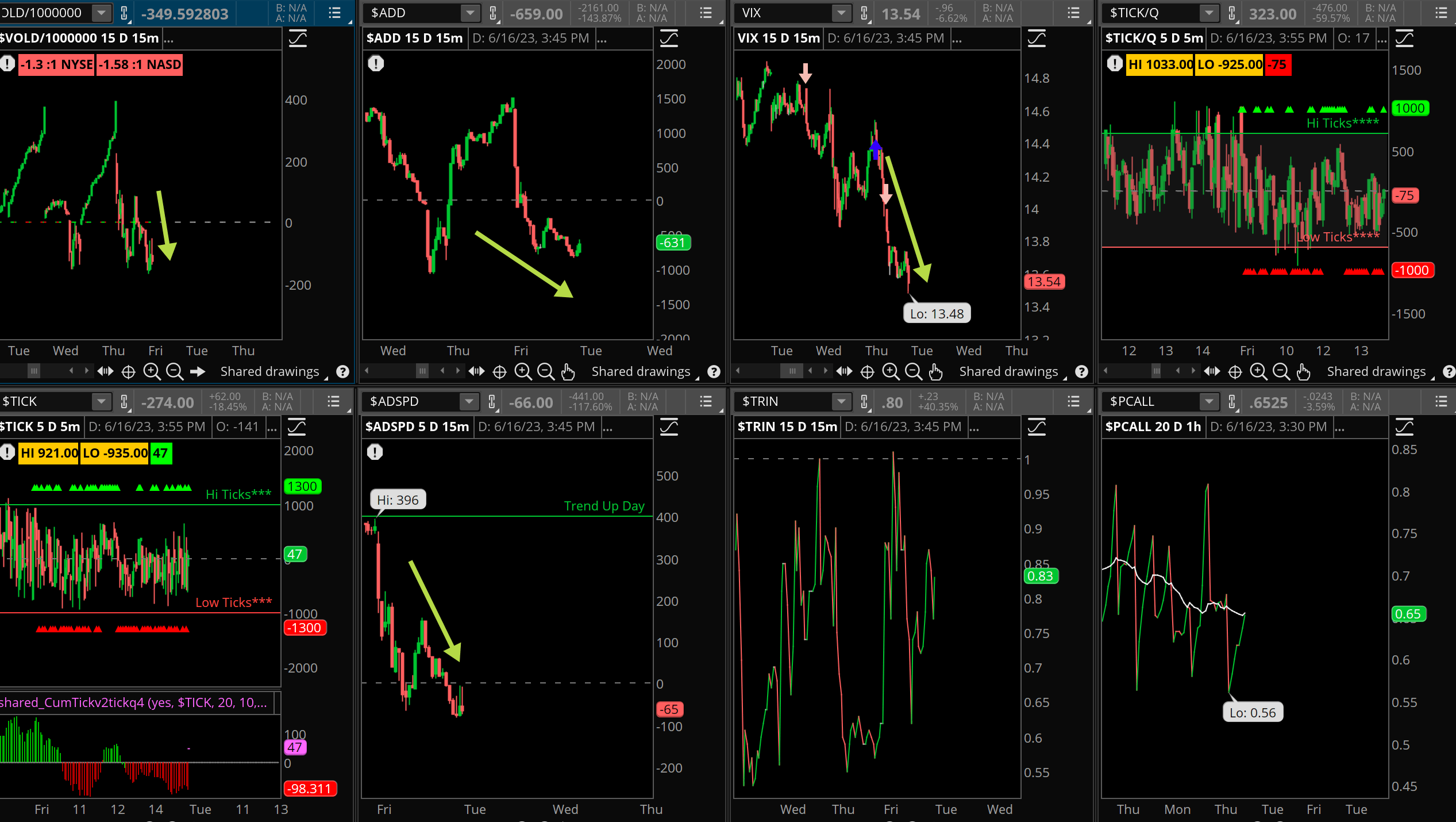

Finally a down session for the markets, though it was not cheered but rather a sign of fatigue. Markets of course do not go up everyday forever, eventually they fall back to earth. The VOLD and ADD were down all session, buyers just not interested on this day. Before a holiday we often see volatility retreat and that happened Friday, the VIX fell sharply under 14%. That’s a danger signal. The ADSPD fell to zero as well, just very little excitement as we approach the holiday weekend.

The Dynamite

Economic Data:

- Tuesday: Housing starts

- Wednesday: Mortgage apps

- Thursday: Jobless claims, Leading indicators, Existing Home Sales

- Friday: June Flash PMI’s

Earnings this week:

- Tuesday: FDX, LZB

- Wednesday: KFY, WGO, KBH

- Thursday: ACN, DRI, SWBI

- Friday: KMX

Fed Watch:

A slew of Fed speakers out this week talking about the economy, inflation and their position on rates. Jay Powell also gives a speech tomorrow, which could be market-moving. With the last meeting just a week ago, I don’t believe there will be anything too earth shattering to shake up the markets.

Stocks to Watch

VIX – With a big drop below 15% last week we’ll see if some of the is burned of with a rise in volatility.

Housing – Some strong results from Lennar and others, we may see a surge in housing data this week as interest rates make their way lower.

Retail – Not much on the news front for retail but this group is due for some outperformance in the summer, we’ll see how this plays out.

[thrive_leads id=’60674′]