The Fuse

Futures are moderately lower today as stocks carry over last week’s bearishness. This is the last trading week of the month and quarter, so far the SPX 500 is up a solid 3.8% in June and 5.85% for the quarter. Plenty of action this week, and as we approach a shortened week. Volatility is on the rise however, as we may see a bit more selling by the end of the week.

Interest Rates are on the rise again as we approach the end of the month. We often see portfolio allocation moves as hedge fund managers look ato balance portfolios. Further, the nagging inflation continues to be a problem for fixed income investors, the inversion may start closing soon. We are watching the 10 year to see if it can exceed 3.85%.

The worry about a coup in Russia was snuffed out this weekend but the markets seemed to be watching it closely. Spanish PPI came out very hot overnight, leading indicators from Japan were down, sentiment in Germany was weak.

The earnings calendar is light this week. Tomorrow am has Schnitzer Steel, after the close we hear from Jefferies and AeroVironment.

We are watching the situation in Europe closely, specifically Russia with a potential military coup at hand. That won’t affect markets too much but any drop for that reason could be a buying chance.

Breadth has been miserable for days and finally rolled over to a sell signal. We are nearly oversold though and that could bring a snapback rally at anytime, but this indicator is bearish.

Volume was elevated on Friday, chalk up another distribution day for stocks. A few more days like this would but the current uptrend in jeopardy.

Good support for the SPX 500 is at 4,300. We could see that area tested this week and a bounce, but as we head into the following week which is holiday-shortened volatility is likely to remain low. That doesn’t mean there won’t be big moves in one direction or the other.

The Internals

What’s it mean?

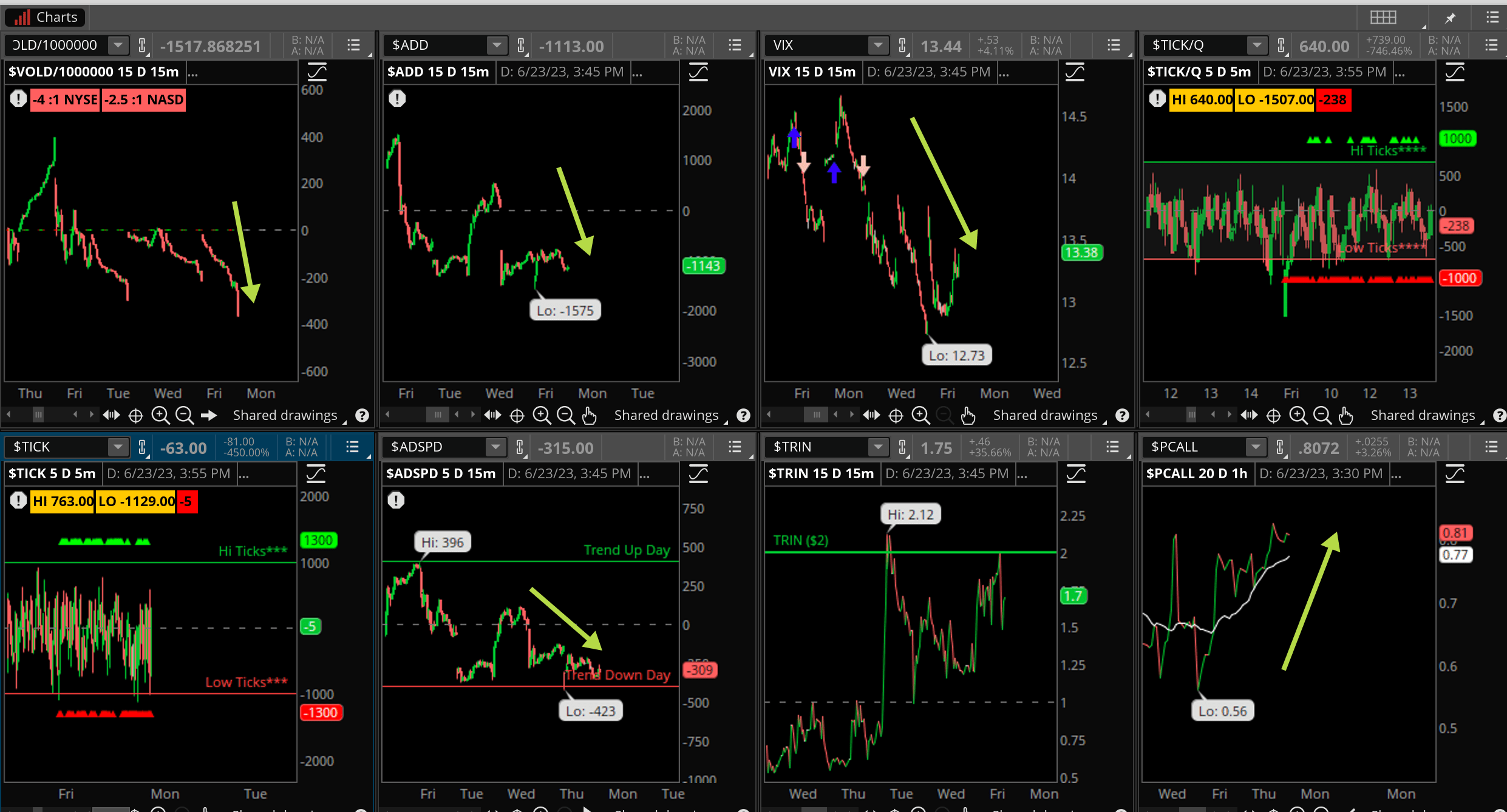

Another day of red arrows. Look at the VOLD in the top left corner. Three straight sessions of heavy selling here as the markets try to gather themselves. The ADD also reflects the bearishness this week, but the put/calls are on the rise here which tells us put protection is being bought. The VIX remains low, hence options (protection) is cheap.

The Dynamite

Economic Data:

- Monday:

- Tuesday: Durable Goods, Housing Price index, Consumer Confidence

- Wednesday: Mortgage Apps

- Thursday: GDP estimate, Jobless Claims, Pending Home Sales

- Friday: PCE, Michigan Sentiment Index

Earnings this week:

- Monday: CCL

- Tuesday: JEF, SCHN

- Wednesday: GIS, MU, BB,HBF

- Thursday: AYI, MKC, RAD, MSC, NKE,

- Friday: STZ

Fed Watch:

More Fed speakers out this coming week. Testimony from Chair Powell on the ‘hill last week was more of the same from the last Fed statement: More hikes coming. Currently about a 75% chance of a hike in July seems about right. Of course, data coming out to start July will change that significantly. Inflation is coming down slowly but may have plateaued, which is why the Fed is going to be more aggressive.

Stocks to Watch

Nike – Earnings coming up this week, we’ll want to hear how inventory levels are progressing along with China sales.

Volatility – Closing under 12% last week showed market players with high complacency. A back up in the VIX means the market may have more downside action.

Window Dressing – It’s the end of the month/quarter and we often see a ‘painting of the tape’, but also profit taking before the month end.

Which will it be, or will there be both? Promises a volatile week of action.