The Fuse

Equity futures are mostly lower this mornings as traders position themselves for the end of the month. For the Nasdaq’s part, May was a great month, so no surprise many are taking some money off the table. Volatility is up a bit after little news to drive stocks up. The stock market remains in a ‘buy the dip’ mode.

Interest Rates are ticking lower today as bond prices rise. Perhaps some position squaring at the end of the month here but nothing in the data is driving rates in either direction. The trend in yield has been higher but rates corrected downward a bit yesterday.

Maybe a debt ceiling deal is closer to the finish line? A committee voted 7-6 to approve, and now goes to a vote in the Congress. Overnight, poor economic data from China pushed European stocks lower, and that has spilled into the US markets. Lots of jobs data to come this week. In addition, three fed speakers, the beige book and PMI will be out.

Not much on the earnings front last night, but we’ll hear from big players Salesforce, CrowdStrike and Okta today, along with Veeva, Nordstrom and Chewy.

It’s the end of the month today and there could be some window dressing. However, we may see bids hold up into the jobs report this coming Friday.

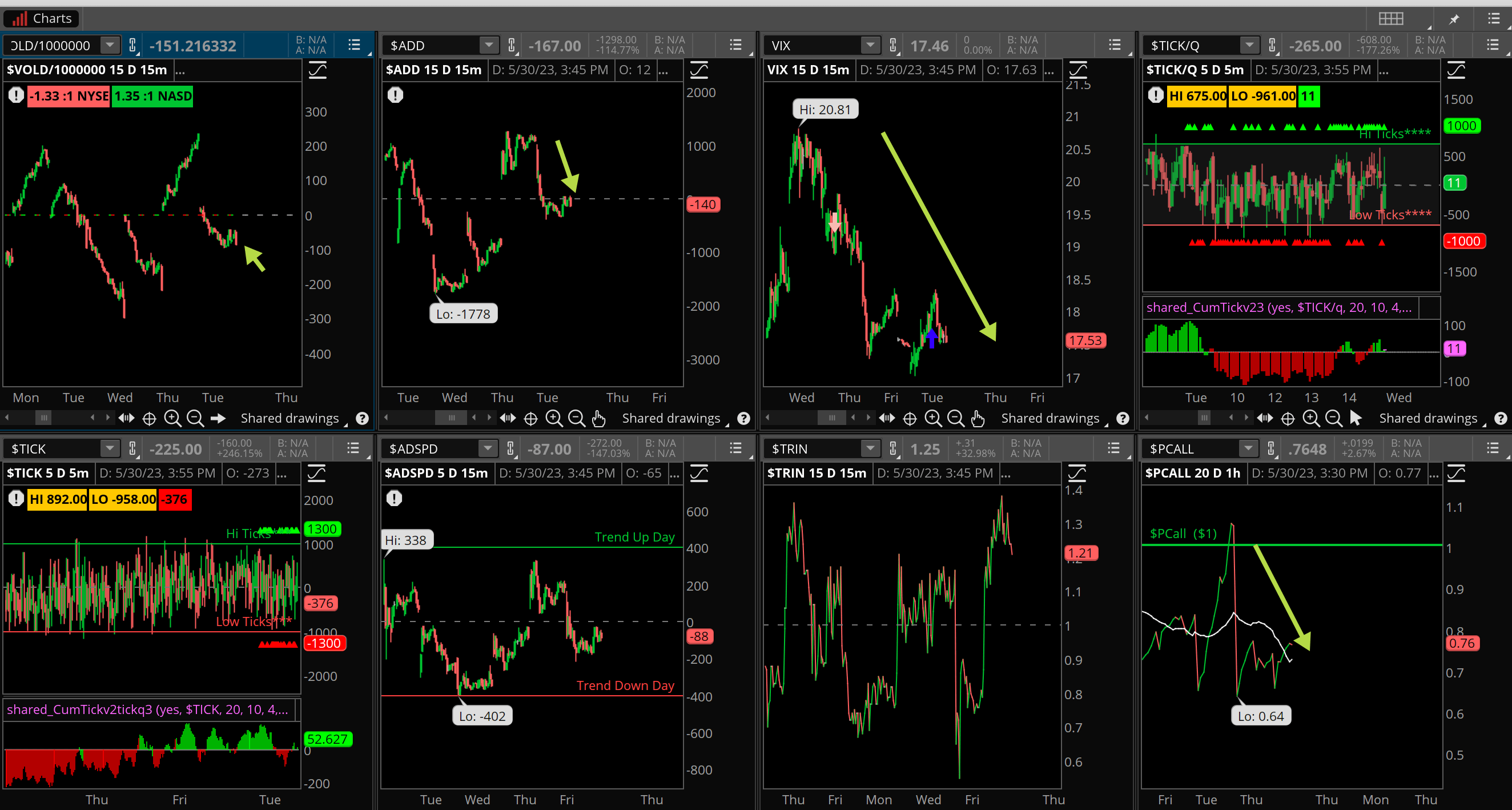

Mediocre breadth today with a slight edge to the bears. It makes sense after last Friday’s bear rout, but we could see things shift later in the week. Some very good action in tech remains to focal point for the bulls.

Volume trends were better on Monday than prior Mondays, and that could be a positive for the bulls leading into June.

We still see 4200 as a tough area for the SPX 500 to crack. However, a weekly close above there changes the chart and technicals dramatically.

The Nasdaq was solid yesterday and remains the leader of the pack, the Nasdaq COMP with a close above 13K.

The Internals

What’s it mean?

A rather blah day as the markets responded early to the news of a debt ceiling raise agreement. But that was short-lived, with a sell the news effect seen in the internals. VOLD was down all session, breadth was weak and finished negatively. Put/calls were down but most of that action was early in the day, ADD was pretty flat. We may see some good action later in the week with the new month starting up on Thursday.

The Dynamite

Economic Data:

- Wednesday:

- Thursday:

- Friday:

Earnings this week:

- Wednesday:

- Thursday:

- Friday:

Fed Watch: The committee cannot be too pleased with the recent inflation data. Susan Collins from Boston will speak twice tomorrow, Patrick Harker a couple times this week with Philip Jefferson tomorrow. We enter a quiet period soon.

Issues/Stocks to Watch this week

Jobs Data – The recent gains in jobs data continue to confound everyone. Can we continue creating so many new jobs at this late stage of the cycle? We’ll find out more this week.

Washington DC – More drama with the debt ceiling issue, perhaps there is some progress this coming week, at least we hope so.

Volatility – The VIX fell hard last week and that often means ‘payback’ after a holiday. We’ll see if that happens and a sell the news event is the result.

[thrive_leads id=’60674′]