The Fuse

Equity futures are soft this morning, drafting on the losses overnight in Europe. In Beijing, stockholders were told NOT to sell any stocks, and that stock market has risen 11% today. For the US markets, it’s been a strong month of November, the indices are posting their best numbers since July 2022.

Interest Rates are moving lower this mornings as investors take a risk off approach following the weekend. There was positive news on the shopping front though and that may drive buyers to start picking up stocks in this group.

Today is cyber monday, a big selling day for retail as the holiday shopping season is kicked off. It was a record online sales figure for black friday buying, up more than 7.5% by most estimates. This is a good start to the holiday shopping season.

Earnings will be in focus this week, today we’ll hear from ZS while tomorrow is a big technology day with CRWD, WDAY, SPLK, HPE, NTAP and INTU.

It’s the last few trading days of November and what a month it has been! Most indices up a staggering amount this month, all on board with the Nasdaq leading the way up about 11% (others up 7% or more). It’s been a broad rally to be sure, with plenty of participation from different groups and sectors. As we start the new month on Friday, we should keep in mind that an overbought market will make it difficult to gain new ground. Friday was a very narrow range of trading, less than 1/4% top to bottom, very small and dangerous.

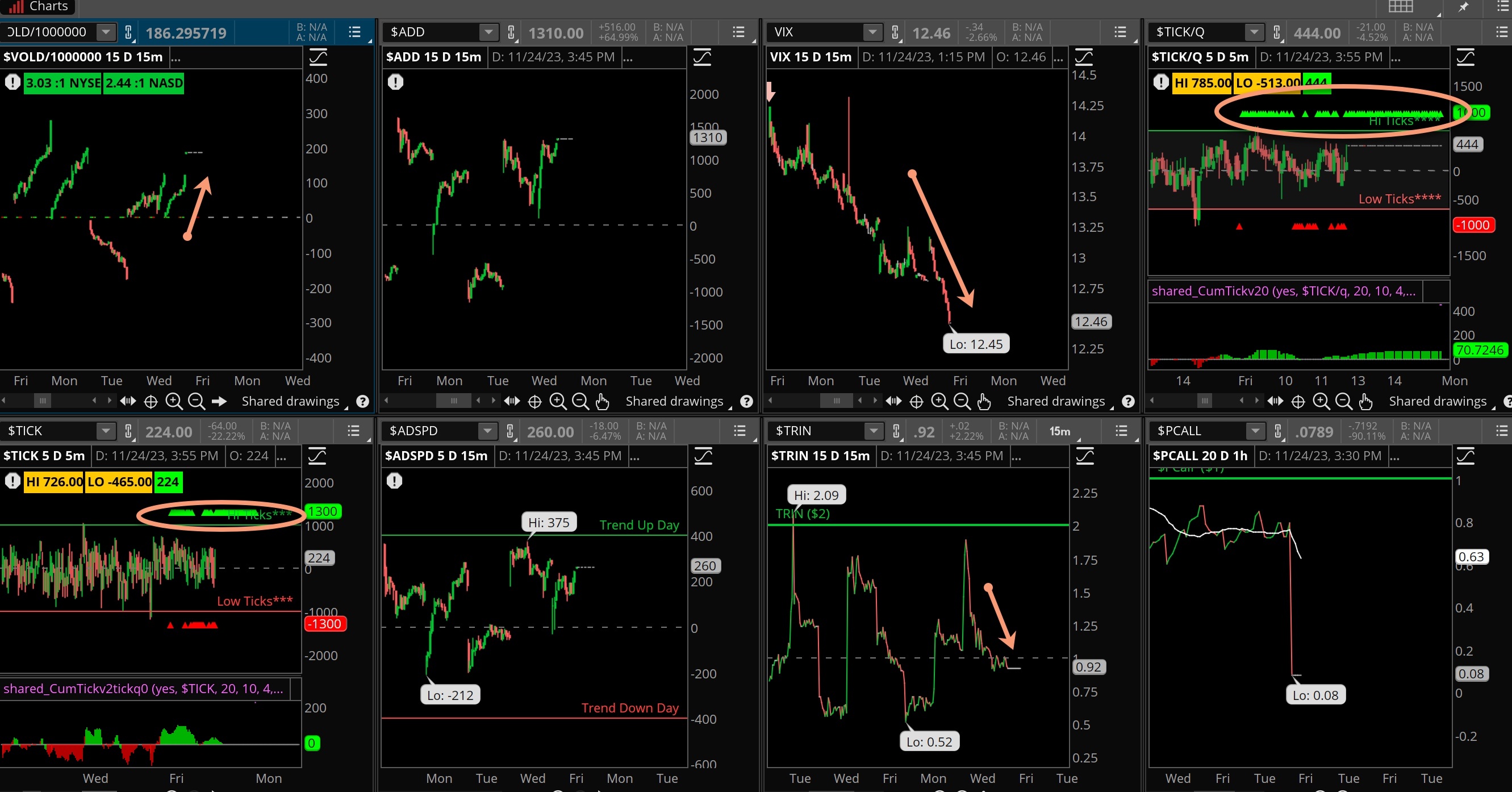

Breadth was very strong and did not reflect the weakness in the overall market price action. However, we did witness the very broad Russell 2K up sharply, nearly 1% on the session which carries plenty of names to skew breadth positively. But it wasn’t only the small caps that performed Friday. Oil/energy were well bid along with commodity names. That’s some good rotation out of the big tech names and may continue.

Volume trends were mediocre as Friday was one of the lowest turnover days of the year. The reason for that is due to a half session, markets closed at 1pm EST. We expect to see much more volume next week as we close the books on November and get the new month started on Friday.

Some good support is still being held at the key 4,400 level on the SPX 500 that is strengthening, the 20 day moving average is now up to 4,395 and climbing higher. This marker will represent good support in a pullback, where from here if the market does correct is just a mild 3% move down. However, if the market remains buoyant and stubborn those shorter term moving averages will move up quickly. We still see 4,600 as the next target to the upside, 1% away.

The Internals

What’s it mean?

What is notable in the octagon above is the very bullish ticks on the Nasdaq and NYSE all session long. We often see sellers come in on a Friday and a more mixed picture in these indicators, but not on Friday. The bulls were defiant. VOLD was strong as was ADD, but the VIX plunged again and sits at a dangerously low level. It won’t take much to turn the markets lower.

The Dynamite

Economic Data:

- Monday: New Home Sales October

- Tuesday: Consumer Confidence

- Wednesday: GDP second estimate, Fed Beige Book, Crude inventories

- Thursday: Jobless Claims, Income/Spending, PCE price index, chicago PMI, pending home sales

- Friday: Global PMI, ISM Manufacturing, construction spending

Earnings this week:

- Monday: ZS

- Tuesday: CRWD, HPE, INTU, NTAP, SPLK

- Wednesday: DLTR, FTCH, FL, WOOF, CRDO, FIVE, OKTA, PVH, SNOW, VSCO

- Thursday: BIG, CBRL, K AMBA, DELL, MRVL, CRM, ULTA

- Friday:

Fed Watch:

Quite a few Fed speakers will be out this week, Five on Tuesday and several later in the week including Chair Powell on Friday. The committee may comment on the recent softer inflation data but will likely be paying close attention to the PCE number released on Thursday along with income/spending. Markets are not expecting a hike in December, only a 4.5% chance of that happening but is pricing in the first rate cut in June 2024. We expect to hear the committee’s comments this week to continue the hawkish statement of ‘higher for longer’, holding out for the possibility to hike rates just in case.

Stocks to Watch

Volatility – The VIX is at its lowest levels of the year and that represents a dangerous situation. We’re not calling for a rise here, in fact the VIX can stay latent for some time but with so many uncertainties that may arise out of nowhere it makes sense to have some put protection on hand.

Retail – It’s been a big weekend for holiday shoppers but we have Cyber Monday coming up and the first full week of shopping for the season.

Expectations are high for most companies this holiday and into the new year.

Technology – It is an unusually high volume week for technology earnings, with CRM, OKTA, DELL, SNOW, and CRWD, HPE, INTU coming up with earnings and guidance. Most of these charts are strong and have been solid winners in November, but it’s all about the future and how they see things turning in 2024.