The Fuse

Equity futures are a bit soft as the overbought condition continues to burn off. Volatility is creeping higher but is still at a very complacent level under 13%. Several fed speakers out today may help move markets.

Interest Rates are slightly higher on the long end of the curve as we wait to see how treasury auctions play out later in the week.

European stocks fell overnight for a second straight down session pointing to a weaker open for US stocks. Crude oil is higher by 1% as the market considers more rate cuts from OPEC while gold remains buoyant above 2K per ounce. The day after Thanksgiving is often a down session and the crowd did not disappoint.

Earnings last night from ZS were strong but the hot money is leaving the name. PDD put up a huge beat and is higher by more than 10% this morning. Later today we’ll hear from INTU, WDAY, CRWD, SPLK, HPE, NTAP and a few others.

Stocks fell modestly yesterday on better turnover but not overwhelming. Holiday shopping is off to the races and is looking pretty strong, several retail names (Amazon included) were higher yesterday. The bond auctions yesterday, a concern for many was decent, not great. Buyers stepped in but we’ll have bigger size coming out later in the week.

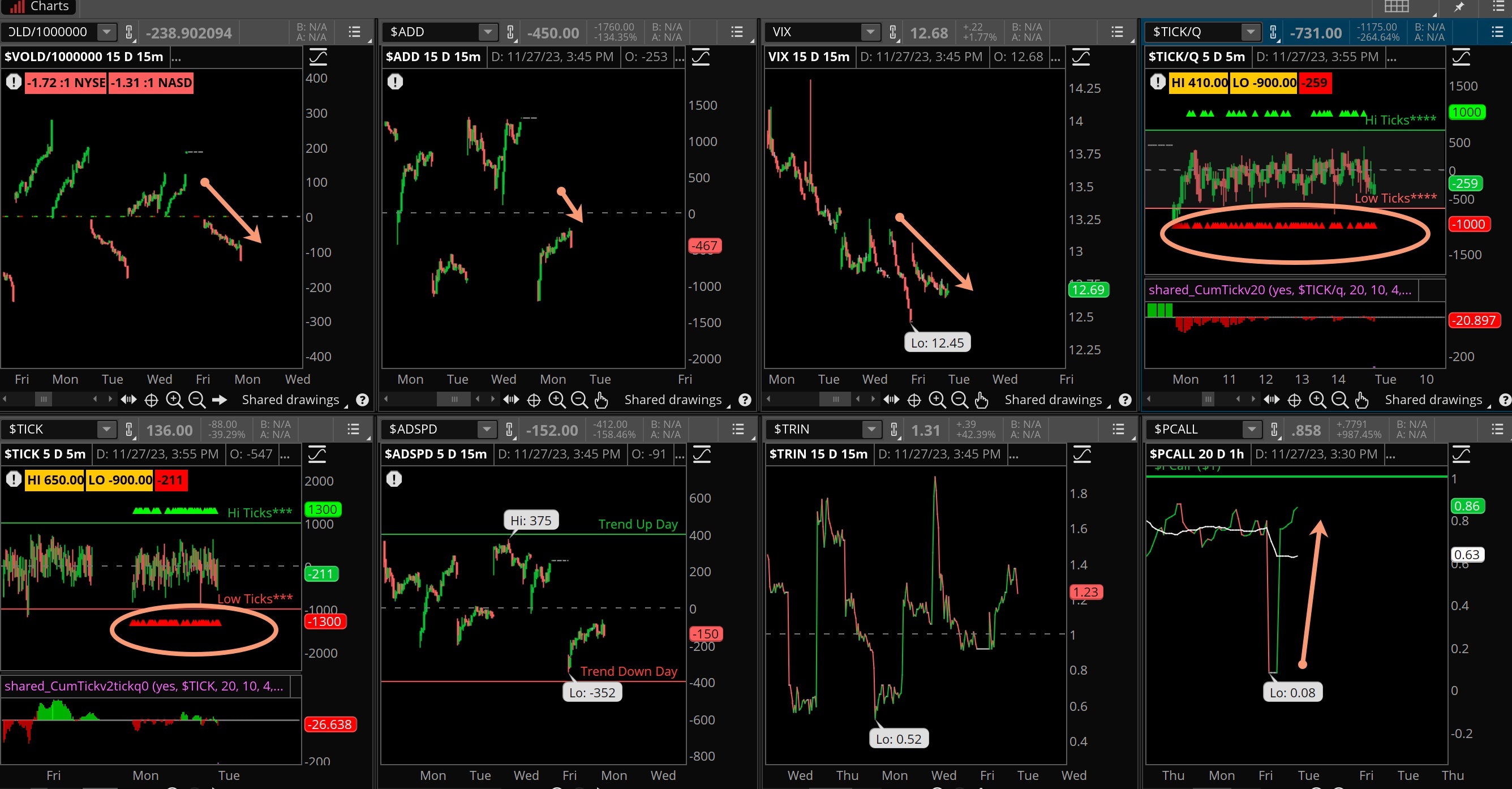

Breadth was weak all session long as it appears Friday’s strong breadth brought out the overbought sellers. That’s fine, the bulls would say as long as there is no followthrough to the downside. All in all, it wasn’t horrible breadth, as we saw a few pockets of strength in tech and retail.

Considering Friday was only a half-day trading session it wasn’t hard to beat the volume number yesterday. While we technical should call a down session on higher volume a distribution day, what matters most is how the markets handle the rest of the week. We might see the pace picking up as we come closer to month end.

A bit of a pullback as the indices fall back into their recent bases. That’s not a bad thing, especially since the oscillators were very overbought at the close Friday. We still have good support at 4,400 and a few gaps to fill on the way down there, 4,600 is the magic number to see if a run towards the old highs is in order.

The Internals

What’s it mean?

Let’s call Monday’s consolidation a whole bunch of nothing. Yes, the indices fell a bit but the losses were contained. A list traders returned to their desks and decided to play some gains, taking out stops high/low without much consequence. VOLD was down all session but we may see a turnaround Tuesday, so be ready for that. VIX remians muted but rose slightly, ticks were mixed but we can see evidence of selling during the session. After Friday’s mindless day we did have a bit of volatility, normal after a holiday session. We’ll see more later in the week.

The Dynamite

Economic Data:

- Tuesday: Consumer Confidence

- Wednesday: GDP second estimate, Fed Beige Book, Crude inventories

- Thursday: Jobless Claims, Income/Spending, PCE price index, chicago PMI, pending home sales

- Friday: Global PMI, ISM Manufacturing, construction spending

Earnings this week:

- Tuesday: CRWD, HPE, INTU, NTAP, SPLK

- Wednesday: DLTR, FTCH, FL, WOOF, CRDO, FIVE, OKTA, PVH, SNOW, VSCO

- Thursday: BIG, CBRL, K AMBA, DELL, MRVL, CRM, ULTA

- Friday:

Fed Watch:

Quite a few Fed speakers will be out this week, Five on Tuesday and several later in the week including Chair Powell on Friday. The committee may comment on the recent softer inflation data but will likely be paying close attention to the PCE number released on Thursday along with income/spending. Markets are not expecting a hike in December, only a 4.5% chance of that happening but is pricing in the first rate cut in June 2024. We expect to hear the committee’s comments this week to continue the hawkish statement of ‘higher for longer’, holding out for the possibility to hike rates just in case.

Stocks to Watch

Volatility – The VIX is at its lowest levels of the year and that represents a dangerous situation. We’re not calling for a rise here, in fact the VIX can stay latent for some time but with so many uncertainties that may arise out of nowhere it makes sense to have some put protection on hand.

Retail – It’s been a big weekend for holiday shoppers but we have Cyber Monday coming up and the first full week of shopping for the season.

Expectations are high for most companies this holiday and into the new year.

Technology – It is an unusually high volume week for technology earnings, with CRM, OKTA, DELL, SNOW, and CRWD, HPE, INTU coming up with earnings and guidance. Most of these charts are strong and have been solid winners in November, but it’s all about the future and how they see things turning in 2024.