The Fuse

Equity futures are sharply higher this morning as Euro stocks climbed overnight and as we come towards the end of the month, always some bullish window dressing occurs (in a bull market trend). Fed Governor Waller suggested the central bank’s current policy is well-positioned to bring inflation down to it’s 2% objective.

Interest Rates are lower on the long end of the curve early this am, we’ll be watching the bond auctions later in the day. Gold is flat while crude oil is up roughly 2%. However, gasoline prices have fallen more than 60 days in a row to $3.25 per gallon. Consumers welcome the drop into this very heavy shopping season.

News overnight of the passing of Charlie Munger, long time Berkshire investor and best friend to Warren Buffett for more than 5 decades.

He was a giant in the investing industry with an irreverent style and wit like no other.

Strong earnings last night from CRWD and WDAY have these stocks ripping higher this morning. Also we heard good things from NTAP, which is moving sharply higher as well. This morning a solid beat finally from FL has this stock up nearly 5% but poor results from Dollar Tree is pushing this stock lower.

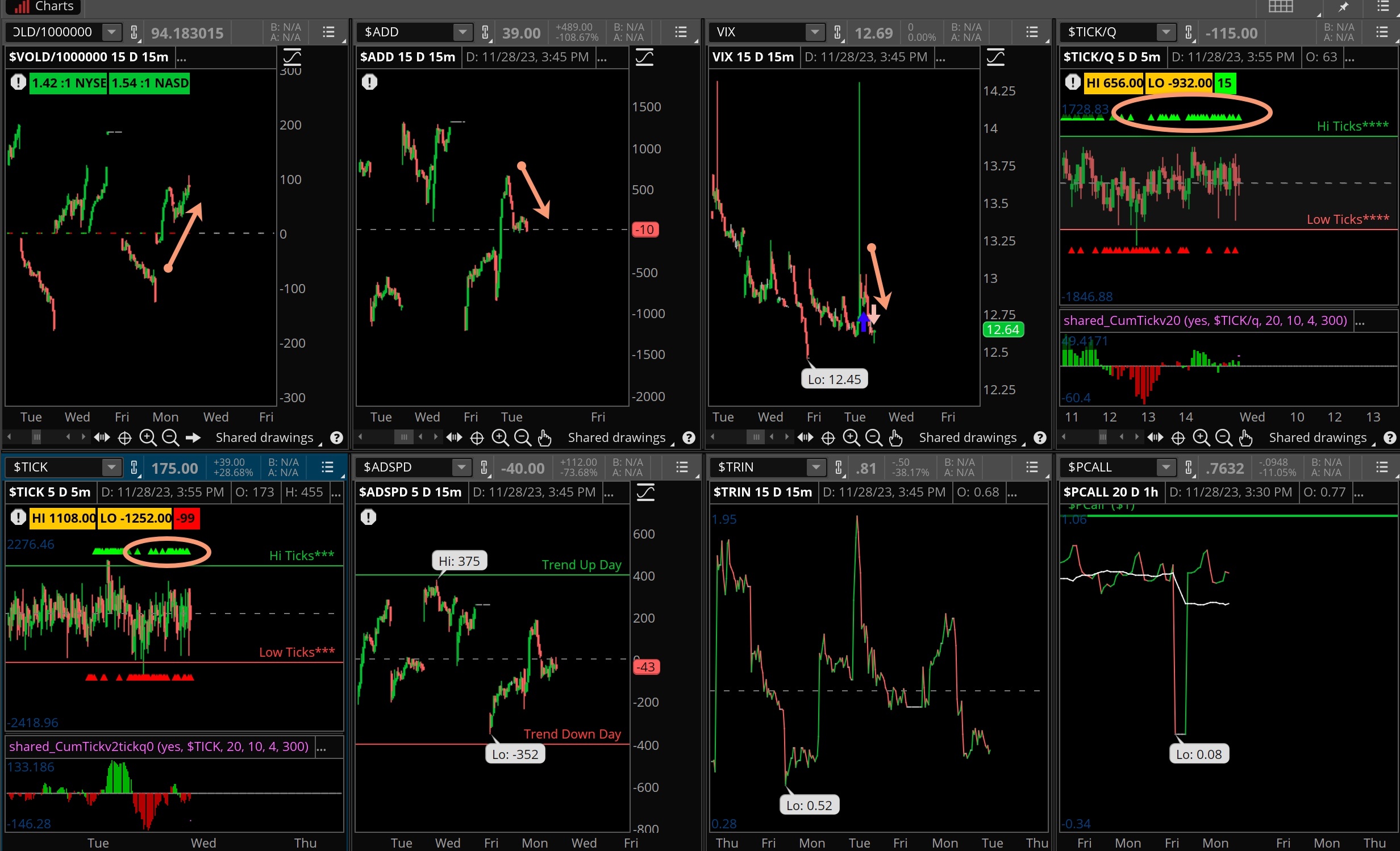

It was a volatile session with the indices falling sharply at one point, rallying hard and then selling off end of day to finish the session with modest gains. Winners barely outpaced losers while turnover was weak once more, but some Fed speakers did manage to raise some eyebrows.

Breadth was slightly positive but it points to an exhausted buying situation, and if there is little buying left then all we have are sellers, and that means the markets will drop. Further, the low VIX shows high complacency even during a seasonally strong period.

Volume trends continue to be bullish and in fact the SPX 500 and Nasdaq both posted accumulation days. Of course, there needs to be a series of these to underscore the upside action, and with month end coming up and the start of a new month (thur/fri) we could see the bulls take charge again.

It seems like 4,600 and 4,500 are like kryptonite to the markets. Buyers won’t take the market up and sellers lack the conviction to bring it lower. Of course, seasonality is in the bulls’ favor now until the end of the year, so the high end may get warmer sooner rather than later.

The Internals

What’s it mean?

Not much of anything here as the internals were mixed all day long. The VOLD was up but barely, the ADD was on the flat line while ticks were pretty well distributed all session. Put/call was muted and the VIX remains dangerously low. With some earnings and more fed speakers this week along with the end of November there could be some movement in the internals by week’s end.

The Dynamite

Economic Data:

- Wednesday: GDP second estimate, Fed Beige Book, Crude inventories

- Thursday: Jobless Claims, Income/Spending, PCE price index, chicago PMI, pending home sales

- Friday: Global PMI, ISM Manufacturing, construction spending

Earnings this week:

- Wednesday: DLTR, FTCH, FL, WOOF, CRDO, FIVE, OKTA, PVH, SNOW, VSCO

- Thursday: BIG, CBRL, K AMBA, DELL, MRVL, CRM, ULTA

- Friday:

Fed Watch:

Quite a few Fed speakers will be out this week, Five on Tuesday and several later in the week including Chair Powell on Friday. The committee may comment on the recent softer inflation data but will likely be paying close attention to the PCE number released on Thursday along with income/spending. Markets are not expecting a hike in December, only a 4.5% chance of that happening but is pricing in the first rate cut in June 2024. We expect to hear the committee’s comments this week to continue the hawkish statement of ‘higher for longer’, holding out for the possibility to hike rates just in case.

Stocks to Watch

Volatility – The VIX is at its lowest levels of the year and that represents a dangerous situation. We’re not calling for a rise here, in fact the VIX can stay latent for some time but with so many uncertainties that may arise out of nowhere it makes sense to have some put protection on hand.

Retail – It’s been a big weekend for holiday shoppers but we have Cyber Monday coming up and the first full week of shopping for the season.

Expectations are high for most companies this holiday and into the new year.

Technology – It is an unusually high volume week for technology earnings, with CRM, OKTA, DELL, SNOW, and CRWD, HPE, INTU coming up with earnings and guidance. Most of these charts are strong and have been solid winners in November, but it’s all about the future and how they see things turning in 2024.