The Fuse

Equity futures are mixed this morning after a very bold move up on Thursday which included some very solid market statistics. We have had a nice run higher this week, more than 200 SPX 500 points since the low of 4,103 on Friday and now we are pretty well overbought.

Interest Rates are moderately higher after yesterday’s major move down in yield on the long end of the curve. That helped to stoke a strong rally in equities, even high yielding debt rallied significantly.

More attacks by Israel have spawned concern for this weekend, but given the lack of worry markets are complacent and feeling as if any new attacks will just be in stride. Investors/traders are focused on the markets at this point.

Decent earnings beat from Apple but with the usual cautious guidance, they sold a record amount of iPhones for the quarter and are upbeat about the coming holiday season. Square/Block posted strong numbers and guided up as did DraftKings last night, Fortinet is getting hammered though after missing earnings.

Fallout from the Fed decision/meeting was pretty positive. Overseas markets ‘ran with it’ and posted strong gains as well. Economic data is coming in Fed friendly again, with good productivity and negative unit labor costs.

Thursday was one of the best up sessions in quite some time, with more than 8-1 positive issues. That’s pretty amazing after such a strong move earlier in the week, but now the oscillators are pretty well overbought.

A second straight day of strong turnover had the bulls toasting after the close. This strong move on solid volume signals the big institutions are back and buying stocks once again.

The 4300 level was taken out Thursday but what’s important is to hold that level for the weekend. Markets are now severely overbought in the short term and a corrective move can happen at any moment. Markets don’t go up everyday forever and when very fast moves happen like this they tend to trap people who come in late.

The Internals

What’s it mean?

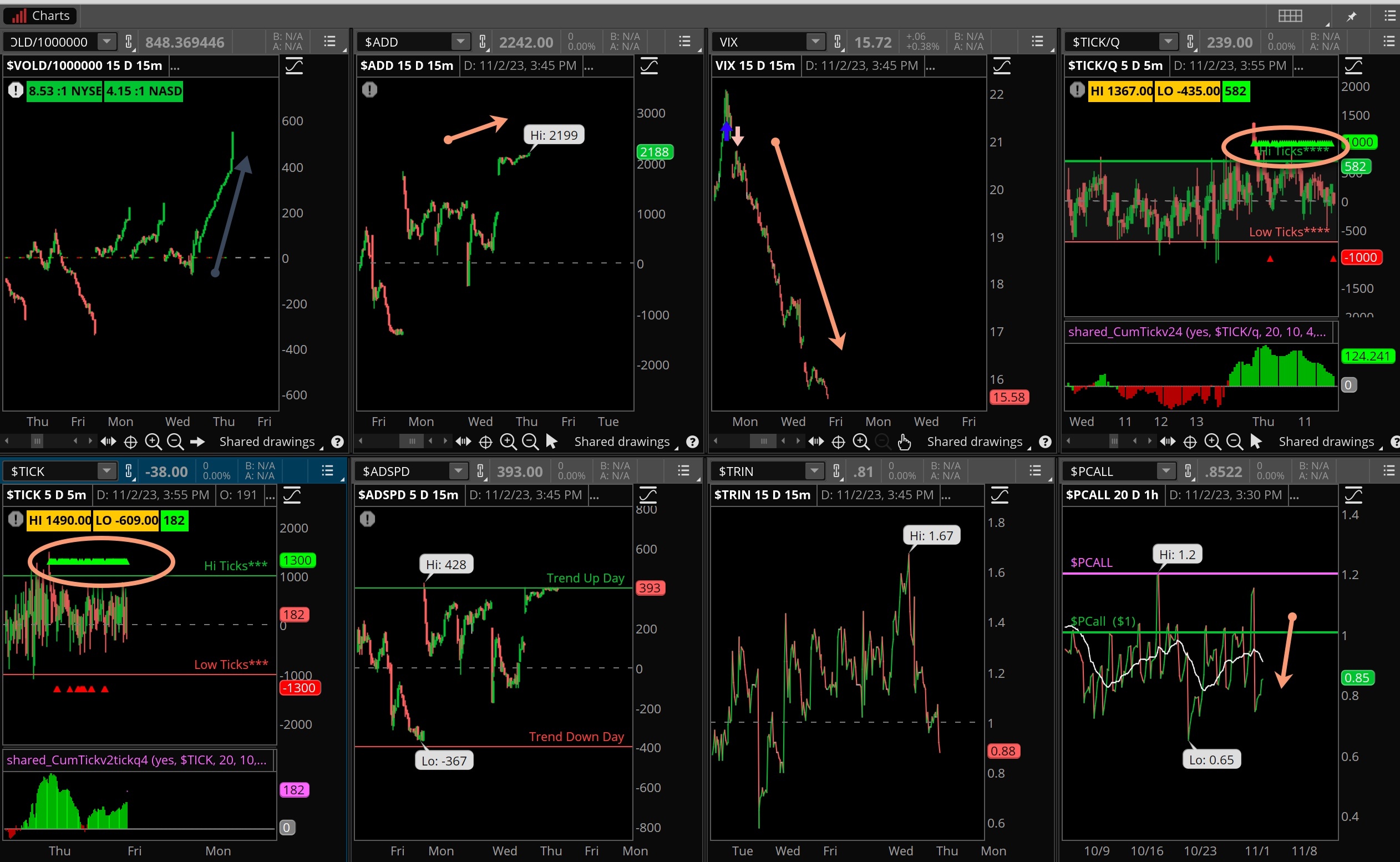

It was a rout of the bears from the start, and if you needed some evidence just look at the dominance in the ticks. Green all day long, ver few red ticks to be seen, a rarity over the prior couple of weeks. Along with the ticks we saw the VOLD shoot higher all day and finish at the highs of the session, also very impressive. VIX took another tumble and now sits below 16% which reflects high complacency, we’ll see if that burns off before Thanksgiving approaches.

The Dynamite

Economic Data:

- Friday: NFP employment report, Global final PMI, ISM, non-manufacturing index

Earnings this week:

- Friday: AMC, AXL, CAH, DOC, CBOE

Fed Watch:

The committee gave the investing public what they wanted – and that was no move on rates and a slight hint they could be through with rate hikes. The caveat of course was that the group could at anytime raise rates, but Chair Powell stated he was comfortable that current policy was creating tighter monetary conditions. That said, they were pleasantly surprised by the strong GDP report last week.

Issues/Stocks to Watch

Apple – The biggest company in the world will release earnings on Thursday, everyone will be watching/waiting with great anticipation. The stock chart is horrible at this point after a severe 20% correction. Will good earnings change that and turn the chart bullish again?

Federal Reserve – It’s time for another interest rate policy decision, the committee is likely to pass on a hike this week but will continue to keep the door open for more hikes. Last week’s inflation numbers were not Fed friendly. I expect to hear the Chairman and the committee reiterate their commitment to snuff out inflation and do whatever it takes. As Powell once said, ‘there is going to be pain’.

Interest Rates – Will the news releases this coming week help to bring bond buyers back or will the 10 year finally get a week over the 5% level and stay there for awhile?