The Fuse

Futures are up nicely this morning following strength overseas in Europe. Stocks are finishing up the month of November in grand style.

The SPX 500 will finish up more than 8% this month, about the same for the Russell 2K while the Nasdaq sports a double digit gain.

Interest Rates are modestly higher this morning as bond sellers take some profits following some nice gains in November. Yields are still pointing lower.

Elon Musk had an interesting interview last night on the Dealbook stage, it’s being talked about and the impact on social media and Tesla. Former Secretary of State Henry Kissinger died at the age of 100. Eurozone inflation dropped to 2.4%, more than expected.

Very strong earnings last night from Salesforce has that company up sharply today, more than 10%. Also solid numbers. from Synopsis and Snowflake rounded out a solid tech trio of earnings, Five Below beat and raised their guidance as well. This morning we hear from Kroger and Big Lots while tonight it is Ulta, Marvell, Dell and Ambarella among others.

Stocks fell flat yesterday but there was a surge of buying early in the session as the pullbacks continue to be bought. Given today is the last day of the month expect more window dressing as fund managers seek to show good performers on their month end tally sheet.

Breadth was pretty strong yesterday with winners beating losers by a 2-1 margin. That’s almost enough to get this indicator onto a buy signal, one more day might do it. With Chair Powell set to speak twice on Friday there could be some excitement.

Turnover was better again on Wednesday but the price action was not, hence we cannot label this session an accumulation day, but certainly the churn was evident. As the week comes to a close, the bulls would like a very positive finish to the month on good turnover.

The SPX 500 made a run at 4,600 but fell a bit short of that target. Nevertheless, buyers still are showing interest at higher prices, and eventually these ceilings will be probed as long as markets are not too overbought. The Russell 2K led the way, hence the better breadth while the Nasdaq fared poorly.

The Internals

What’s it mean?

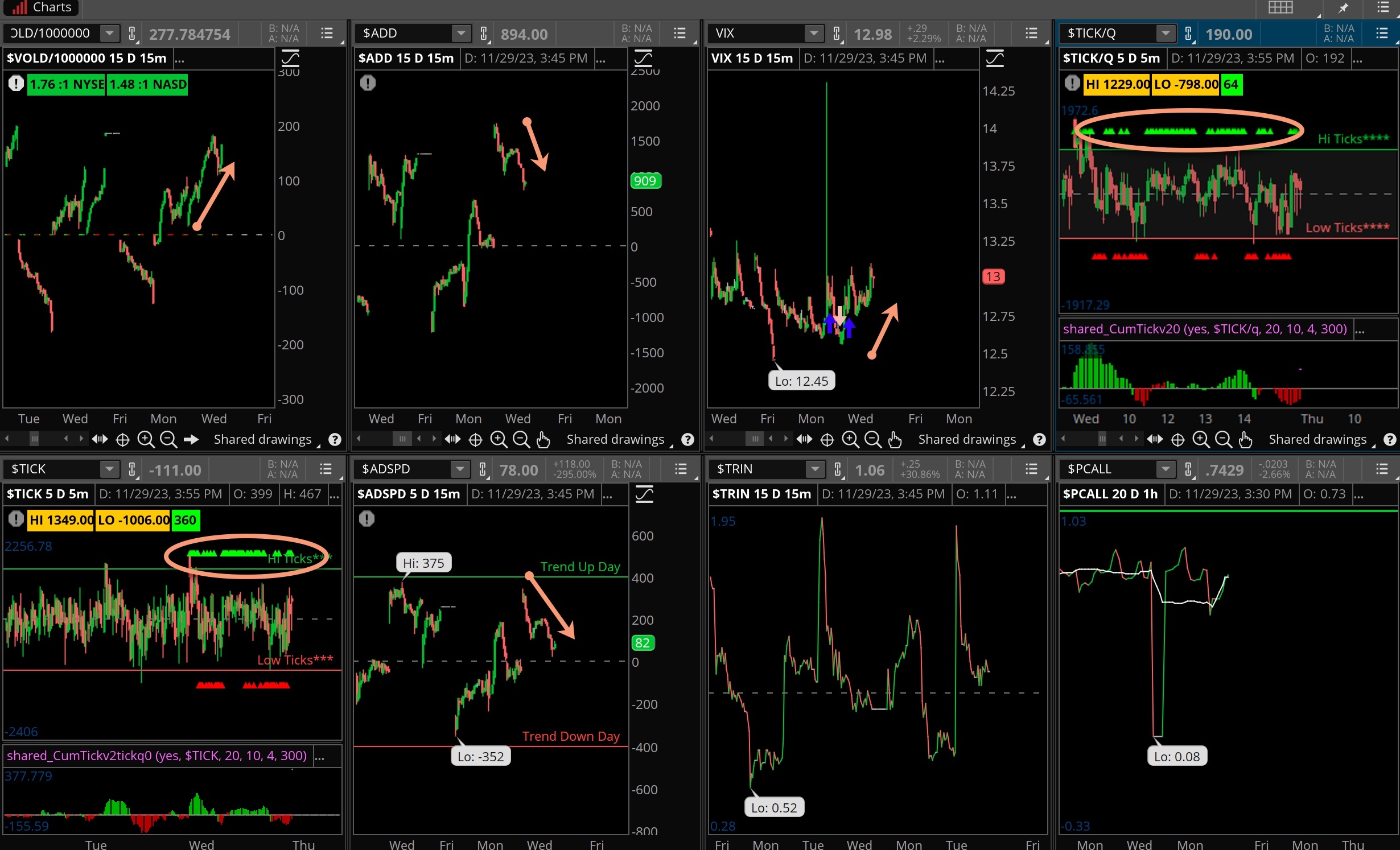

Another mixed session for the internal indicators as the VOLD showed strength but the ADD and ADSPD were down. That is a negative divergence but can be corrected over the next day or so. Ticks were mixed but mostly green on a down day, that would be considered a positive divergence. Something for everyone!

VIX was a bit higher on the day, about 1% but still remains under 13% – a dangerous level.

The Dynamite

Economic Data:

- Thursday: Jobless Claims, Income/Spending, PCE price index, chicago PMI, pending home sales

- Friday: Global PMI, ISM Manufacturing, construction spending

Earnings this week:

- Thursday: BIG, CBRL, K AMBA, DELL, MRVL, CRM, ULTA

- Friday:

Fed Watch:

Quite a few Fed speakers will be out this week, Five on Tuesday and several later in the week including Chair Powell on Friday. The committee may comment on the recent softer inflation data but will likely be paying close attention to the PCE number released on Thursday along with income/spending. Markets are not expecting a hike in December, only a 4.5% chance of that happening but is pricing in the first rate cut in June 2024. We expect to hear the committee’s comments this week to continue the hawkish statement of ‘higher for longer’, holding out for the possibility to hike rates just in case.

Stocks to Watch

Volatility – The VIX is at its lowest levels of the year and that represents a dangerous situation. We’re not calling for a rise here, in fact the VIX can stay latent for some time but with so many uncertainties that may arise out of nowhere it makes sense to have some put protection on hand.

Retail – It’s been a big weekend for holiday shoppers but we have Cyber Monday coming up and the first full week of shopping for the season.

Expectations are high for most companies this holiday and into the new year.

Technology – It is an unusually high volume week for technology earnings, with CRM, OKTA, DELL, SNOW, and CRWD, HPE, INTU coming up with earnings and guidance. Most of these charts are strong and have been solid winners in November, but it’s all about the future and how they see things turning in 2024.